Atlas Salt Inc. (TSXV: SALT), Breaking the Ice on Supply

Published on 2026-06-30

Atlas Salt Inc. is a junior mining company focused on developing Newfoundland’s Great Atlantic Salt project and positioning itself for the sale of de-icing salt into eastern Canada and the northeastern United States. Typical junior mining projects lack insight into project completion, have highly unstable demand environments, face steep permitting hurdles, and lack any competitive differentiation factors which make the majority of gold, copper, silver, uranium, and other metals juniors essentially uninvestable in our view. In spite of being pre-revenue and largely pre-financing, Atlas Salt differs from these projects fundamentally and poses the potential for tremendous returns with a remarkably strong line of sight. Atlas Salt is essentially fully permitted, is poised to sell into stable demand in a critical services market, is building a mine with a remarkably simple design making it easily executable on a relative basis, and thus has a very high probability of securing project financing and executing on an ‘infrastructure like’ mine. Current SALT share prices are not indicative of Great Atlantic’s high likelihood of success, stable nature upon operation, or the additional upside posed by inferred reserves and persistent rock salt price inflation. As a result, we believe the shares offer a tremendous risk-reward proposition at current levels.

De-icing salt, Atlas Salt’s only proposed avenue of generating revenue, is a staple product across cold climates worldwide, and for good reason. In the United States alone, over 150,000 car accidents occur annually due to icy conditions, killing an average of 1,300 people per year. For reference, 227 U.S. military troops died per year from 2006-2021. The prevention of such deaths is undoubtedly one the major priorities of the United States annual ~US$840B in military spending, painting a clear picture for the monetary value which governments may impose on the safety of their citizens.

For readers who live in temperate climates, de-icing salt works in a very simple way: pebble sized pieces of salt are spread across cement surfaces, either in anticipation of snow or after it has fallen, in order to limit the amount of ice and snow which is left on roadways, sidewalks, and pathways. Due to its chemical composition, salt both absorbs water and drastically lowers its freezing temperature, making roads dryer, less icy, and significantly safer. Studies completed in Ontario have indicated that de-icing salt decreases the number of collisions on four-lane highways by 93%, and on two-lane highways by 42%. Combine this effective nature with the ease of access to salt as a cheap commodity, and de-icing salt emerges as a simple but remarkable solution to the problem of unsafe winter driving conditions with no economic substitutes.

In aggregate, demand for safety of roadways by governments, as well as safety of personal and commercial walkways by consumers and industrial agents, amounts to US$4.5B per annum, and is expected to reach US$6.8B by 2034 (~5.3% CAGR). Of this US$4.5B in annual demand, over 50% of spending comes from the northeastern United States and eastern Canada; areas of dense populations, complex and prominent roadways, sophisticated governments with significant safety obligations to their citizens, and, most importantly, lots of snow, sleet, and freezing rain. Cities like Boston, New York, Pittsburg and Montreal all conjure an image of busy streets and cold, wet weather: it does not come as a surprise that they consume the majority of the world’s de-icing salt in aggregate.

Atlas Salt plans to deliver salt to this major sub-market, the northeastern United States and eastern Canada, and is strategically positioned to do so. In this report, we will review the demand dynamics in this market, the supply dynamics and competition which Atlas faces, the Great Atlantic Salt project at depth, the governance team leading SALT towards production, and lastly consider share valuation and related key drivers of project value creation.

Demand Dynamics

The northeastern United States and eastern Canada are estimated to consume in the range of 28.5-36.0 million tonnes of de-icing salt per annum. De-icing salt serves a clear economic purpose and has zero financial demand as compared to gold, silver, or other mined commodities. As is such, demand is stable, predictable, and over a multi-year period is essentially guaranteed given the lack of economical substitutes for the product and the government safety mandates which drive most of demand. Demand is not a function of any broad-scale economic events (barring a government collapse, in which case any equity is likely not particularly attractive), but is simply a function of roads needing maintenance and poor weather returning every year.

While the majority of de-icing salt demand stems from government purchases, significant portions of volumes also flow through consumer and industrial customers at up to 5-6x higher end market pricing.

Figure 1: Consumer De-icing Salt

Source: Scotwood Industries

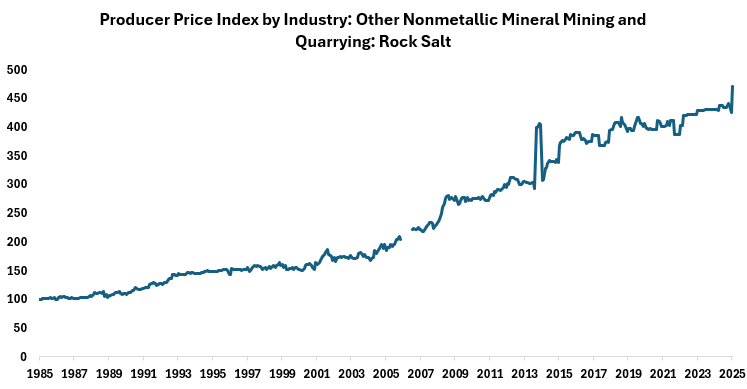

Although demand for de-icing salt is unaffected by economic changes, one factor does impact short-run demand: weather patterns. The entirety of annual de-icing salt demand is consumed during winter months, and the temperature and precipitation levels during these months can be variable. In spite of weather variance, the largest year-over-year drop in U.S. rock salt prices over the last 40 years is ~3% as per FRED data (annualized price increase of 4% per year over the same period). Since 1985, rock salt prices have only fallen two consecutive years on two occasions and have never fallen in three consecutive years. Figure 2 shows the U.S. PPI index for rock salt pricing from 1985-2025. Clearly short-term weather variance does not have significant and durable impacts on demand, but perhaps long-term weather changes could.

Figure 2: Historical Rock Salt Inflation

Source: FRED, Phi Research

From an anecdotal analysis of this graph two trends emerge. Firstly, rock salt pricing is stable and has never been subject to short term price collapses or persistent downward trends. Secondly, prices are consistently growing. Given the stability of supply to the market, which we will discuss in detail later on, it is easy to infer that incremental demand growth has been the driver of these price movements over time.

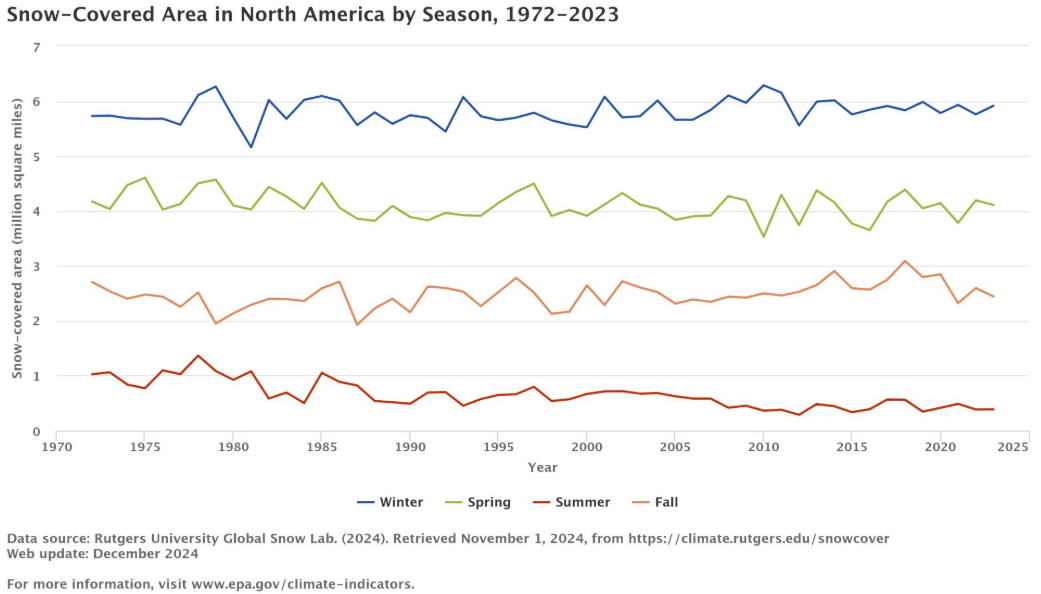

The scientific consensus at present is that global climates will face significant changes on a go forward basis due to greenhouse gas emissions, and that climates have already changed significantly due to the same drivers. Although this perspective is frequently politicized and debated, an investment thesis does not have room for ideologies, only facts. We know that U.S. rock salt pricing has grown at a steady mid-single digit pace over the previous 40 years based on inflation data. What else we know is that from 1972-2023, the snow-covered area in North America has been unchanged in the winter, spring, and fall seasons, the only seasons in which material demand for de-icing salt stems.

Figure 3: Historical Snow-Covered Area in North America

Source: EPA

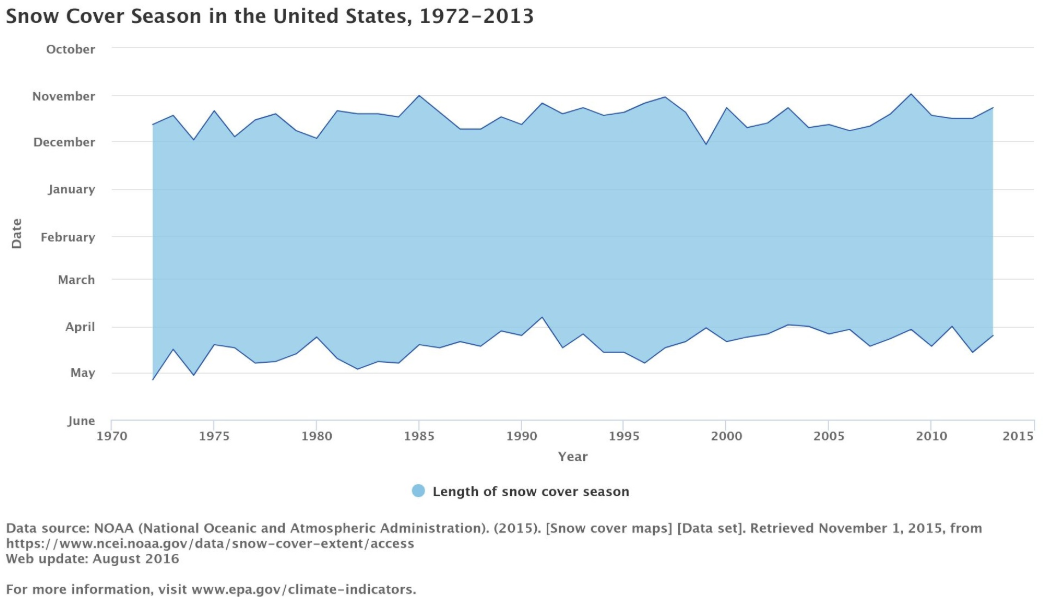

In addition, the season of snow coverage in the United States, or the length of the de-icing salt demand season, has also remained unchanged from 1972-2013. Figure 4 shows the length of the snow coverage season in the United States as per EPA data.

Figure 4: United States Snow-Coverage Season

Source: EPA

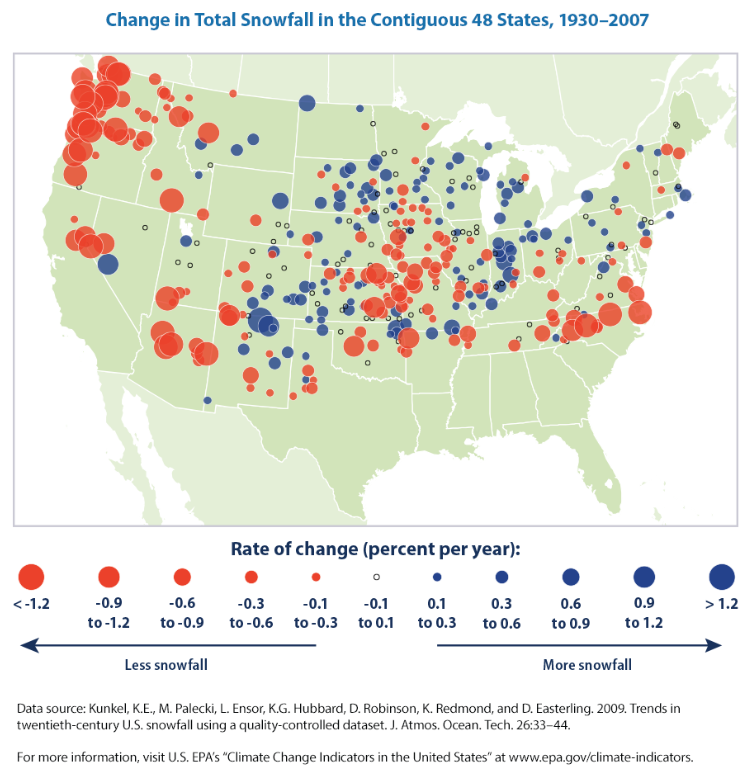

A final piece of relevant historical data we have found is on the annual rate of change in annual snowfall from 1930-2007 (Figure 5). The Pacific Northwest, Central United States, and areas of North Carolina and Tennessee have indeed seen significant negative changes in annual snowfall over the observed period, however these changes are not within SALT’s targeted market. In the Midwest, New York, Massachusetts, and Pennsylvania, snowfall rates have been flat or increasing at the majority of weather stations over the long term.

Figure 5: Total Annual Snowfall Rate of Change – 1930-2007

Source: EPA

Predicting weather is notoriously difficult in both the short term and long term; there is a reason that it is one of the easiest things for people to make conversation over. What we can see in regards to demand for de-icing salt is this: demand in SALT’s market has historically risen, and snowfall rates, the snow covered area, and the length of the season of snow coverage have historically been very stable over the long term in spite of persistent greenhouse gas emissions. SALT’s current feasibility study only accounts for 25 years of production, meaning that even if these trends do diverge on a century long time frame, effects to the Great Atlantic Salt project will be essentially nil. Given this background, the lack of economical substitutes to salt, and the primary driver of demand being safety, it is difficult to paint a picture of the future where demand for de-icing salt deviates from what it has been historically: stable and slowly growing. Placed in the context of a supply side that has been stagnant for decades (more below), and the result is a modestly bullish outlook for de-icing salt sales.

Supply Dynamics

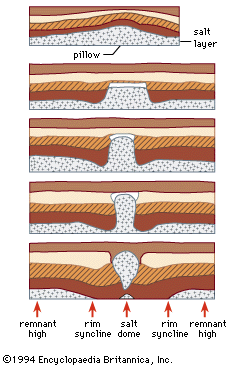

Salt, in various forms, is plentiful on Earth. For the sake of supplying salt to its markets, three prominent methods exist: evaporated recovery of sea salt, solution mining, and conventional mining, with the lion’s share of de-icing salt stemming from the last method. Underground salt deposits typically take two forms, salt domes and salt beds. Salt beds form underground from the evaporation of ancient, isolated bodies of saltwater, forming a thick and laterally persistent layer of salt between layers of rock. At shallow depths, these layers of salt remain intact, and can be mined with good economics due to their depth and continuity when salt layer thickness is sufficient (this is the setup for the Great Atlantic Salt project). When salt beds are buried to greater depths and at greater pressure overtime, they often begin to be ‘squeegeed’ upwards through discontinuities or cracks in overhead rock layers, seeking a lower pressure environment and migrating due to salt’s inability to compact (material density has a low maximum). The result of this migration is a salt dome (Figure 6), a large dome of salt at a much shallower depth than its corresponding salt bed. At times, salt can actually be pushed all the way to the Earth’s surface, forming salt glaciers (an interesting phenomena worth a Google search after finishing this report).

Figure 6: Salt Dome Formation

Source: Britannica

Although not liquidly traded like gold or oil, salt is a global commodity, and cost of delivery is the only factor driving the efficiency of supply. Two factors drive cost of delivery: mine operating costs and shipping and handling costs. Mine operation economics vary by project, however due to the geological prevalence of salt globally the true driver of efficient supply boils down to shipping and handling costs. The cheapest way to deliver salt, as is the case with any bulk commodities, is by boat, making proximity to large waterways a significant cost advantage for a salt operation as this eliminates expensive trucking costs. For mines located proximal to waterways, the distance from export to import terminal still has a significant impact on cost of delivering.

Despite these facts, roughly one-third of North America’s de-icing salt demand is fulfilled by imported volumes from Chile, Egypt, and other far-off lands. This amounts to ~8-10 million tonnes per annum (Mtpa) of supply which incurs an additional ~US$20-30/ton in shipping costs (government end market sale price is ~US$100/ton). In addition, imported volumes operate on 3-4 week lead times due to the distance which imports must travel and other logistical challenges from importing from distant markets with less trade interconnection. This is in the context of winter storms which may only be forecasted days prior to demand requirement spikes.

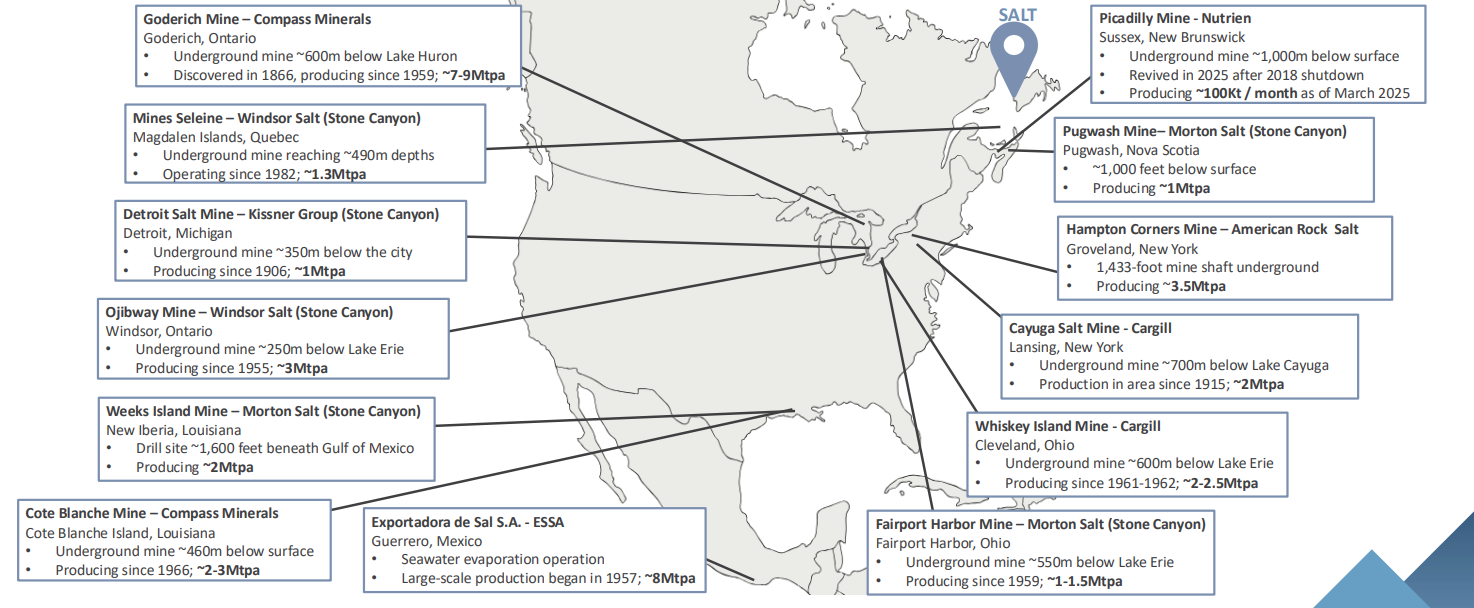

In many ways it is puzzling that such a large portion of supply stems from foreign sources given their structural cost disadvantage. North America does feature a number of producing salt mines (Figure 7), however no new development has flowed to the space for nearly three decades (other than the restart of Nutrien’s Picadilly Mine, produces ~1.2 Mtpa). Note that in this period of dry development, (2000-2025), U.S. rock salt prices have risen at an annualized rate of ~5% per annum, well above inflation levels of ~2.5% annually.

Figure 7: Summary of North American Salt Mines

Source: Company Presentation

The main reason driving an inefficiently high amount of supply to stem from foreign markets is established North American mines nearing end of life and expansion of current projects being limited. The only currently proposed investment in mine development in North America is at Compass Mineral’s Goderich Mine (largest producer in North America), with proposed investment going towards maintaining current output levels as the mine ages, not on expanding production. More prominently, one of North America’s largest mines, Cargill’s Avery Island, closed in 2022 as a result of mine age and safety concerns. This removed ~3 Mtpa of supply from the market, with no prospective replacement apart from Atlas Salt or foreign imports.

A number of other major producing North American mines are also aging rapidly. Notably, Cargill’s Cayuga Salt Mine is expected to exhaust reserves within five years with permitting for expansion having been denied. This is a result of the mine’s vertical shaft nature and risk of collapse, which also produces a structural cost disadvantage relative to angled access mines (like Great Atlantic Salt). Cayuga is located in central New York, making it a direct competitor to Atlas Salt upon production. Its absence from the market would push North America’s salt imports into the 40-45% of demand range, with a disproportionate amount of the step change stemming from SALT’s end markets.

For lack of a better term (or to make a pun), supply is essentially frozen in an inefficient state and has prospects to move away from efficiency going forward, not towards it. No new North American salt mines have been developed for over 25 years, no new mines are set to be developed going forward (apart from the Great Atlantic Salt project), existing mines have no ambition for production expansion and a significant share of North American supply is set to disappear within five years, all while a large and growing share of demand is met by foreign imports with a structural cost disadvantage. Placed in the context of stable demand and persistent price inflation, and there is clearly a business case to be made around new North American de-icing salt development.

The Great Atlantic Salt Project

Atlas Salt’s Great Atlantic Salt project is a proposed partial solution to the above inefficiencies in the de-icing salt market. Figure 7 above shows the geographic position of Great Atlantic Salt in North America relative to its peers and its proximity to northeastern U.S. and eastern Canadian markets. Clearly, Great Atlantic Salt has a large structural advantage to foreign importers when it comes to reaching Montreal, New York, Halifax, Toronto, Boston, and any eastern seaboard locations by water. Relative to North American peers, it sits between the great lakes waterway and the eastern U.S. coastal cities, meaning it can feasibly sell into both markets. By water, SALT can transport its product to market in ~3 days, fast enough to meet flash demand for winter storms.

Reserves

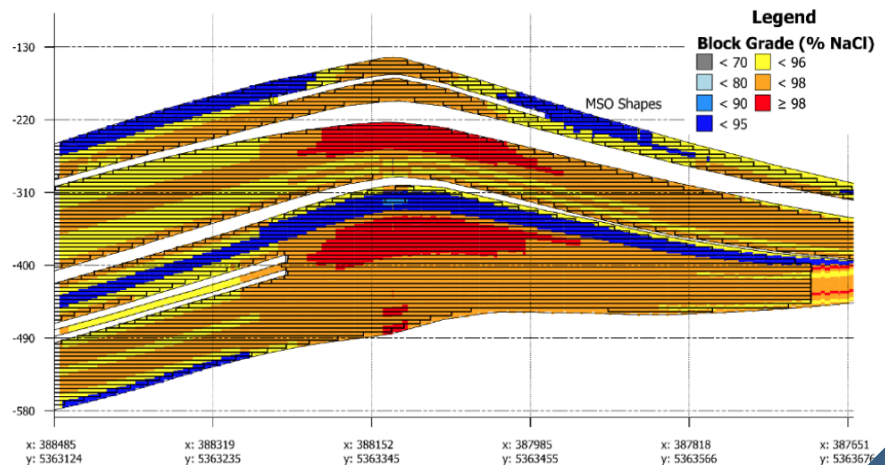

Through 31 drill holes, Great Atlantic Salt has been pegged at 91 million tonnes of probable reserves, 368 million tonnes of indicated reserves, and 827 million tonnes of inferred reserves. Reserves exhibit tremendous lateral continuity with no end of bedding having been discovered through exploratory drilling, providing very strong upside to current reserve metrics. Current reserve thickness averages 200m with significant concentrations of high grade reserves (>98% NaCl) and the majority of reserves in the range of 96-98% NaCl, indicative of a low risk reserve base.

Figure 8: Great Atlantic Salt Reserves

Source: Company Presentation

Reserve numbers represent a 0.24 probable to indicated ratio, an extremely low conversion rate for a bedded reserve like salt or potash with no metallurgical risk, good thickness, and uncapped lateral continuity. For reference, salt and potash deposits generally convert indicated reserves to probable reserves at a rate of 0.85-0.95 due to the simple and predictable geology of bedded deposits. This underpins the conservatism of SALT’s current reserves and instills a great deal of confidence in SALT’s feasibility study which only accounts for the removal of 91 million tonnes of probable reserves over mine life.

Mine Design

As previously alluded to, the Great Atlantic Salt project’s underground operations will be accessed by decline ramp, not by vertical shaft, making it the only North American salt mine to do so. This is possible thanks to reserve’s shallow depths (243-335m) and enables lower capital costs and operating costs compared to peers which is easily observable in other mining industries. Vertical mine shafts require tremendous capital investment upon initial construction, as well as high maintenance capital and operating costs to operate and maintain hoists. On the contrary, Atlas can simply drive machinery underground as you would down a hill on the surface. In addition, conveyor belt systems will be implemented for the removal of salt from underground operations which is much cheaper and simpler than hoisting systems. All underground operations are set to be ran electrically on inexpensive hydro-electric power (substation 1.4km from mine site), which when combined with decline access provides an additional cost advantage relative to peers due to lower ventilation costs. Decline ramp access is also preferrable from a health and safety perspective as emergency egress comes by way of a second vehicular ramp rather than man-cage.

Underground operations are set to follow a room-and-pillar geometry with 17m wide rooms and 25m x 25m pillars, mimicking the operation of all other bedded salt mines globally. Mining is set to be done with three fully electric Sandvik continuous miners, eliminating the need for any explosives, their associated costs and ventilation requirements, and cutting the risk of pillar collapse.

Figure 9: Continuous Miner in Underground Salt Operation

Source: BBC

As compared to metals mines, above ground operations are very simple at Great Atlantic Salt. Once salt is removed from underground operations by conveyor belt, the material’s journey continues in an enclosed belt system either to onsite stockpiles or to a nearby export terminal, Turf Point. Apart from an office and parking lot, SALT’s above ground facility requirements are very limited: no metallurgical infrastructure, no tailings ponds, and essentially no waste produced upon operational startup. This significantly lowers environmental risks for Great Atlantic Salt on a go forward basis, on top of their already approved Environmental Assessment (“EA”).

Geography

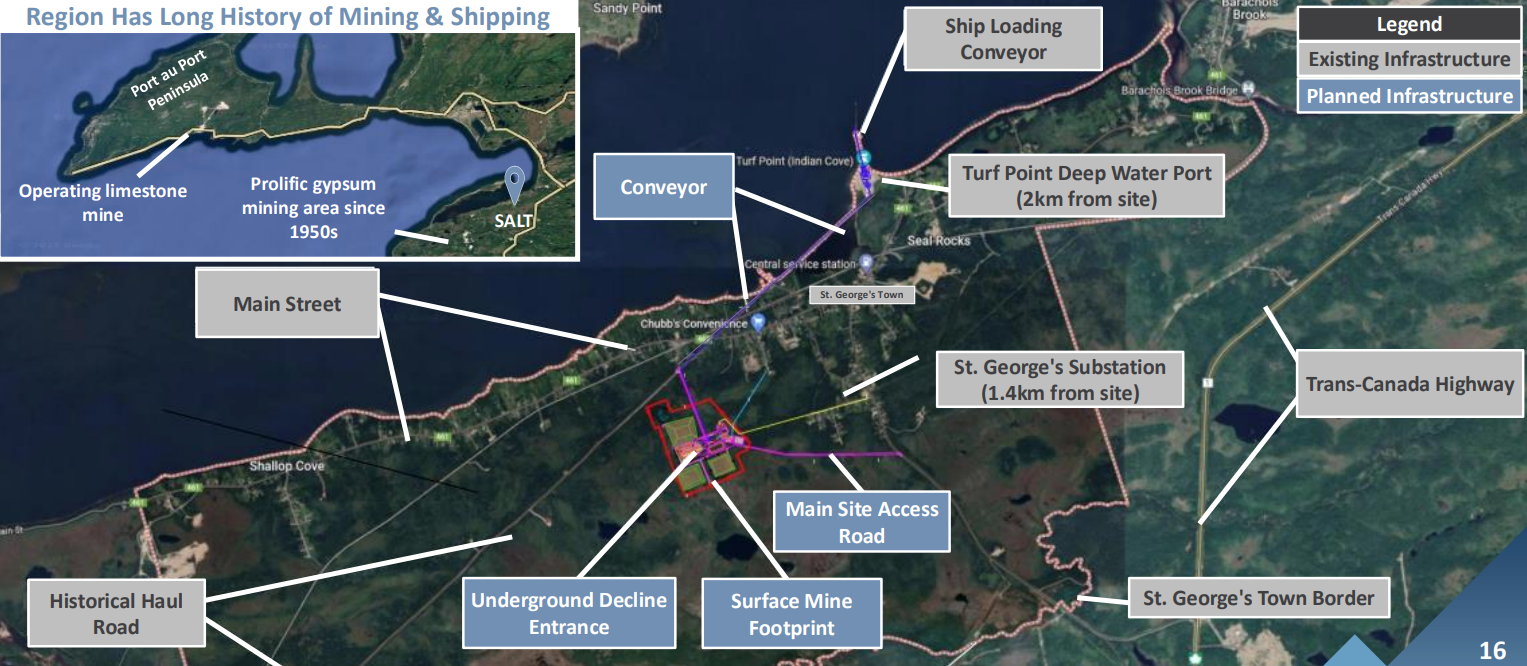

Great Atlantic Salt is located within the town limits of St. George’s, Newfoundland, with Newfoundland & Labrador being known globally as a top-tier mining jurisdiction for a number of reasons. Local and national governments are very friendly to mining operations, largely due to their outsized economic impact on an otherwise stagnant area. On a provincial level, NL has consolidated all permitting to a single department, leading to streamlined permitting timelines like FireFly Metals’ 45 day EA timeline or Great Atlantic Salt’s two month approval process. NL mining policy is friendly, and of equal importance, has been consistent over time. This consistency of policy is vital for underwriters providing financing for decades long projects and bodes well for Atlas Salt’s current situation. Thanks to policy and the continual development of mines across the province, a strong labour pool and individual level culture around mining has developed and can provide consistent, inexpensive, and experienced labour to a project like Great Atlantic Salt.

On a smaller scale, Atlas Salt is positioned for low cost and low risk operations. The Great Atlantic mine site is located proximal to both the Trans Canada highway as well as the Turf Point year-round deepwater port. From a construction perspective, both of these facilities contribute to low import costs, with Turf Point’s proximity also being highly advantageous from an export perspective. St. George’s substation, part of the NL hydroelectric power grid, is located only 1.4km away from the mine site, and access road construction requirements are very limited.

Figure 10: Great Atlantic Salt - Pinpoint Geography

Source: Company Presentation

On a comparative basis, Atlas Salt’s geography lends the project to a smooth construction phase and effective operations post completion. All relevant facilities and cheaply and easily accessible and limited out of mine infrastructure is needed for operations to begin.

Permitting

Permitting is frequently a significant barrier to the execution of greenfield mining projects, however in the case of Great Atlantic Salt the risk appears to be very low at this point. SALT completed its Environmental Assessment with the province in 2024, and as of February 27, 2026, it was confirmed by government that all EA conditions were satisfied for the commencement of Early Works. A subsequent Early Works Development Plan, covering road access, site disturbance, and water management infrastructure has since been approved, making the project shovel-ready when combined with the economic rationale of Great Atlantic Salt’s detailed Updated Feasibility Study (“UFS” - November 5, 2025). Certain activities such as clearing trees and brush and power tie-ins have subsequently commenced.

No major permitting roadblocks remain to Great Atlantic Salt at this point, only minor licenses and registrations such as a pesticides applications license, fuel storage tank registrations, and permits for electrical meters. Great Atlantic Salt has very limited above ground construction requirements and is generally an extremely low impact project, making the likelihood of not securing such minor permits, or the emergence of unforeseen environmental issues highly unlikely going forward. In addition, Great Atlantic Salt’s Environmental Assessment passed the government desk in only two months, with support from local first nations groups and no pushback from non-government parties. We believe this is a tremendous signal for the governmental support of this project, and testament to the relationships and experience of SALT’s management team which we will detail in the next section.

Fundamental geological differences from metals mines and other comparable salt mines, limited construction requirements, lack of metallurgical work and tailings, and easy access to required facilities all position Great Atlantic Salt as lower risk, lower cost, and higher likelihood of success than any comparable project in every measurable way. Although unforeseeable events do occur in greenfield projects, Great Atlantic Salt has left a significant buffer on reserves in its feasibility study, likely undervalued its own resource on a pricing basis (more in the Valuation section), and is boring in the best ways possible: nothing revolutionary is being attempted with the project and a smooth and successful completion of construction and operations seems like the most likely outcome for Great Atlantic Salt, contingent upon the receipt of financing.

Corporate Governance and Management Alignment with Shareholders

Relative to an ordinary company, Atlas Salt finds itself in a unique position as far as corporate governance needs go. The company is small, must remain lean to keep costs in order during an early works stage, and must emphasize the accomplishment of two goals above all else: securing financing and executing construction. In analyzing Atlas’ corporate governance, we want to see two things which increase the likelihood of achieving these goals: 1) management and board members who have explicit success in constructing and financing previous mines, and 2) significant insider ownership to disincentivize excessive dilution during this phase of development.

Insiders collectively own 9.7% of SALT shares at present, both directly and through Vulcan Minerals Inc. (TSXV: VUL), SALT’s exploreco parent company led by certain directors. Although a 2025 Management Information Circular has not been published at present, meaning current CEO pay is not publicly available yet as he was hired in June of 2025, what we can see from the 2024 circular is that pay is reasonable and almost entirely made in share-based awards.

Nolan Peterson – CEO and Board Director

Altas Salt is currently led by Nolan Peterson, CEO and Director since June of 2025. Peterson has played a role in the construction and advancement of a number of significant mining projects over his 20+ year career and holds both a Bachelor of Materials Engineering and an MBA from the University of British Columbia as well as a CFA charter. Peterson’s first major role in the development of a greenfield mine came through New Gold Inc.’s New Afton mine, a greatly successful project by all standards. Artemis Gold’s current Blackwater Gold Project (one year of commercial production to date) was also developed in part by Peterson while at New Gold. The assets which became the Blackwater mine were initially owned by New Gold and were developed from discovery through feasibility work with the help of Peterson prior to their successful sale to Artemis. With New Gold, Peterson also helped to advance the Rainy River mine to being shovel ready before moving into a role as New Gold’s Operations Controller. Rainy River was a messy project for New Gold; development costs were ~40% over budget as a result of problems with unexpected peat and clay layers above the mine’s pit, as well as a required redesign of tailings operations.

After his time at New Gold, Peterson moved into a position as Operations Controller at TMAC Resources, with responsibilities in developing the Hope Bay Gold Project. Although reserves and the mining process at Hope Bay were successful, issues arose from a metallurgical perspective post-production, and the project was closed for reassessment prior to TMAC’s sale to Agnico Eagle Mines. Since being sold to Agnico Eagle, the Hope Bay project has been reassessed and is being expanded in order to overcome the high fixed costs associated with Arctic operations. After TMAC’s sale to Agnico Eagle, Peterson continued in his role as Operations Controller for a short time before accepting a role as the Chief Executive Officer at World Copper Ltd. With World Copper, Peterson led the successful merger of Cardero Resources, and led and delivered a PEA Study on the company’s Escalones project before leaving his role in 2023.

Peterson’s career has granted him a clear and unique blend of skills. He has accrued a tremendous amount of experience in bringing mines from the discovery phase to operation as both an engineer and on the financial side. Not every project he has participated in has been a tremendous or outsized success, but issues have stemmed from pit design, tailings, and metallurgy design, factors which are not in play at Great Atlantic Salt. Ultimately, unforeseeable negative events occur in mining finance, and appropriately assessing these risks is closer to a valuation sensitivity problem than it is an exercise of faith in management. For a company of this size and in this stage Peterson appears to be a very strong choice for an executive with a long history of mine development experience and corporate finance pedigree. In addition, Peterson speaks very well and has done a tremendous job of promoting the SALT story thus far, closing a $15.2M equity offering in June of this year, an $8.7M offering in October of 2025, delivering an Updated Feasibility Study which doubled expected mine output in November 2025, and securing LOI’s from export credit agencies for major project financing as well as an MOU for $132M of equipment financing with Sandvik.

Robert Booth – Vice President, Engineering & Construction

Robert Booth is in place with SALT to serve a very specific role: direct the construction of Great Atlantic Salt and ensure a smooth transition to operations. From 1990-2017, Booth was employed by Vale S.A., the world’s largest producer of iron ore and pellets. Booth served as a Project Manager from 2004 onwards and oversaw the construction or expansion of a number of Vale’s projects from this point forwards. The first was the 2004 expansion of Vale’s Creighton mine for which Booth managed the deepening of operations from 7,530 feet to 7,820 feet, effectively expanding shafts and building new lateral developments. Booth then spent three years in corporate senior engineering roles before beginning as project manager on Vale’s Totten mine. Totten was a historical shaft which was set to be revamped after being out of operation since 1972 (38 years out of operation), with the 4,130 foot timbered shaft having been flooded since 1976. Somewhat unsurprisingly to us as an outside party, the project was over budget due to poor timber and concrete condition in the historical shaft, as well as delayed due to the global financial crisis, but upon operation no problems were incurred. Booth led operations at Totten for two years prior to serving as Project Director on Vale’s Copper Cliff Mine Project. Booth led Copper Cliff through feasibility work before ending his tenure at Vale. Before joining Atlas Salt in 2023, Booth also spent two years consulting on HudBay Minerals’ Snow Lake expansion. Operations at Snow Lake were grown significantly, on time, and under budget with the assistance of Booth.

Booth clearly has a very deep understanding of mine construction and engineering processes and has been forced to solve the exact problems he will be expected to mitigate at Great Atlantic Salt for decades past. Outside of Totten, he has a tremendous track record of executing projects on budget and on time. At Totten, execution risks were extremely high given refurbishment of what was a flooded ~40 year old mine shaft, a risk which is not comparable in any way to Atlas Salt’s shallow, bedded deposits in well established geology. We see Booth as one of the largest assets to the Atlas Salt team and as a great choice for an individual who is poised to oversee the physical construction of Great Atlantic Salt.

Andrew Smith – Project Director & General Manager

Andrew Smith joined Atlas Salt in 2023 after a decade of work in mine design and project management for Agnico Eagle Mines, Newmont, and Dumas. With Agnico Eagle, Smith contributed to mine design as well as drill and blast design. With Newmont, Smith was once again responsible for blast design, stope conceptuals, and assisting in ventilation work. Smith then spent six years with Dumas, a third party mine construction contractor. With Dumas, Smith served as Manager of the Project Management Office, which in practical terms means negotiating construction related contracts, settling related disputes, and ensuring the proper financial analysis and planning is put into construction operations. Smith will take on what is essentially an identical role with SALT and appears to be well qualified to fulfill his duties of overseeing mine construction on a corporate level, while also assisting Booth with engineering work.

SALT’s management team is currently very lean: this is essentially the entire stack of senior individuals who are set to deliver on the Great Atlantic Salt project. Although we could see headcount increasing appropriately as construction ramps from currently small operations, we believe the current team has the core competencies and past experience in place to execute on what is likely a straightforward build. From a financing perspective, Peterson will be the catalyst for marketing the project, a role which we believe he is capable of fulfilling in conjunction with mining project finance advisors Endeavour Financial.

Board of Directors

SALT’s board of directors is comprised of six members, five of whom are independent (CEO Nolan Peterson being the non-independent member). Select independent directors are profiled below, full board and management profiles can be found here: (link).

Patrick Laracy – Chair of the Board of Directors

Patrick Laracy founded Vulcan Minerals Inc. (TSXV: VUL) in 1995 and has served as the company’s President, CEO, and Director since. Vulcan has endeavoured on a number of exploratory geological projects in Newfoundland and Labrador since founding, spinning out Atlas Salt in 2012 and retaining a 24% equity interest as well as a 3% royalty on project revenues. Laracy holds a Bachelor of Science in Geoscience, an LL.B. in Natural Resource Law and a P.Geo certification. We see Laracy’s tenure in Newfoundland and Labrador geology and associated relationships as a significant asset for SALT.

Rowland Howe – Director

Rowland Howe served as Mine General Manager of Compass Mineral’s Goderich mine, North America’s largest salt mine, from 1995-2011. Howe led the expansion of Goderich from 3.5 million to 7.5 million tonnes per annum, and currently serves as President of the Goderich Port Management Corporation. We view Howe’s experience at Goderich as extremely valuable to Atlas given the geological similarities between Great Atlantic Salt and Goderich and Howe’s associated engineering tenure.

Other independent directors are Bob Kelly, P.Geo and past President and Construction Manager at the Iron Ore Company of Canada, F. Carson Noel, LL.B., seasoned mining consultant, and Governance Director for CIM Newfoundland and Labrador, and Fraser H. Edison, current President and Chairman of Rutter Inc. and member of the board and governance committee of Newfoundland and Labrador Hydro.

Valuation

Great Atlantic Salt’s headline project numbers are a shareholder NPV of $920M and an IRR of 21.3%. 21.3% is an IRR above typical potash project hurdle rates in the 15-20% range and is within the range of successful metals projects of 15-30% despite the stability of salt pricing and Great Atlantic’s low-risk bedded geology. At today’s closing price of $1.55 per share, SALT’s fully diluted market cap sits at $205.7M, only 0.22x project NPV. Trading at a discount to NPV is normal for a company at this stage for a number of reasons. Firstly, there is a risk that the project is not completed due to lack of financing or construction problems - broad scale surveys have shown that ~45-50% of mineral discoveries reach production. Second is a timeline discount: even projects which will reach production in the future do not often begin construction tomorrow. Lastly is the potential for variance between the market’s evaluation of project NPV relative to technical report results. Absent these forces, the only thing driving large discounts in share value to NPV is information asymmetry – the ultimate opportunity for outsized risk adjusted returns.

On a simple anecdotal level, we think that SALT’s current discount to NPV is excessive. If ~50% of mineral discoveries reach production, on a peer-based probability weighted basis, junior mining projects should trade at ~0.5x NPV when excluding construction risks and timeline discounts. Great Atlantic Salt faces significantly lower construction and overrun risks as compared to peers at similar points in project progress, implying they should see a lower discount applied to a 0.5x NPV baseline as compared to metals projects. In spite of this, metals projects frequently trade in the ~0.4x NPV range after receiving full permitting, despite metallurgical risks and volatile commodity pricing. In addition, a 0.5x NPV baseline is unfairly low; the 50% figure we have referenced is for all mineral discoveries. Those which have completed feasibility work and environmental assessment are significantly more likely to be executed, especially when boasting high IRR’s like Great Atlantic Salt.

Ultimately this anecdotal analysis is insufficient, and for a comprehensive understanding of Great Atlantic Salt we will build a cash flows model of the project, both to stress test technical report estimates and to better understand the risk reward of Great Atlantic Salt.

Discounted Cash Flows Model

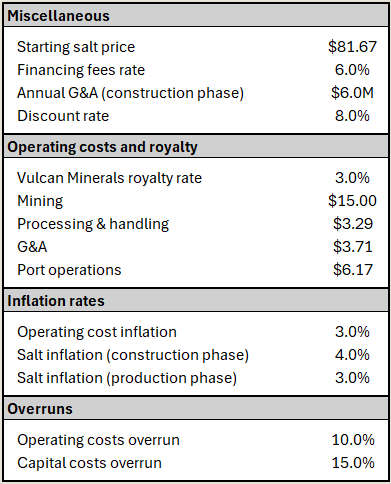

Our discounted cash flows model is constructed using the baseline assumptions from Great Atlantic Salt’s November 5, 2026 NI 43-101 Updated Feasibility Study, a document we suggest investors review on Sedar+ (link). We have modified the assumptions utilized, largely at a discount to the projections given in the technical report, while also accounting for an extended project timeline and the costs of securing financing. Figure 11 shows our baseline assumption set which we will justify below.

Figure 11: Discounted Cash Flows Baseline Assumption Set

Source: Company Filings, Phi Research

Starting Salt Price

Great Atlantic Salt’s UFS utilizes a baseline salt price of CAD$81.67/tonne, which then grows at a chosen inflation level over the project lifetime. This is perhaps the most important assumption made in our model, thus we will rigorously justify our choice of price and ensure conservatism. The only public company who serves de-icing salt markets, Compass Minerals International, Inc. (NYSE: CMP), luckily publishes their own realized pricing levels as well as associated delivery costs. On a CAD/tonne basis, Compass realized pricing of $91.01 in 2025 for government sales (~83% of sales) and $259.39 in consumer and industrial sales. These are both significantly higher than UFS baseline pricing of $81.67 but fundamentally different: UFS pricing assumes sale is realized at SALT’s export terminal, Turf Point, whereas Compass Minerals is vertically integrated and delivers their salt directly to customers. Because of this, Great Atlantic Salt will realize pricing lower than Compass Minerals in order to compensate third-party delivery services. Compass does also publish their shipping and handling costs per tonne of salt, which equate to $36.65 in CAD terms. This estimate may very well be high relative to Atlas Salt, as many of Compass’ operations are in Utah and Louisiana, with Utah shipping and handling costs being incurred via rail and trucking and Louisiana production being routed on a lengthy journey up the Mississipi via barge. Regardless, we can use this information along with details from SALT’s offtake MOU with Scotwood Industries to create our own estimate for realized pricing.

Scotwood Industries (link) packages and distributes rock salt for consumer and industrial de-icing needs (image of packaged product can be found in Figure 1). Atlas and Scotwood’s offtake MOU (link) establishes that Scotwood will utilize 1.25-1.5 Mtpa of Great Atlantic Salt’s 4.2 Mtpa production, and will then package and distribute this salt to locations like Home Depot, Canadian Tire, and other retail and industrial channels. Beyond cost recovery levels, revenues from these sales are to be split 50-50 between Scotwood and Atlas Salt.

Using the midpoint of expected Scotwood offtake, this equates to 33% of Great Atlantic Salt output being sent to Scotwood for retail and industrial sales. We can then assume that the remaining 66% of output is sold to government channels. Using these weightings and pricing information from Compass Minerals, we can then create our own estimate for Great Atlantic Salt’s realized pricing (assuming output started immediately).

To estimate Great Atlantic Salt’s realized government pricing, we simply take Compass Minerals’ realized government pricing in CAD/tonne and subtract their shipping and handling costs in CAD/tonne with an added margin of 10% (assumed profit margin of third-party shipping operators). This is a conservative estimate for two reasons: 1) shipping and handling costs are likely higher for Compass Minerals given some of their operations being in Utah and Louisiana, and 2) SALT’s end markets like New York tend to exhibit some of the highest de-icing end prices (e.g., $127.23 CAD/tonne in Manhattan as compared to Compass’ corporate average of $91.01 CAD/tonne), while also having expectations for significant inflation in 2026/27 winter pricing as compared to the 2025/26 winter (link). Note that Morton Salt’s winning bid of $99.86 USD/ton for New York City in the winter of 2026/27 represents a ~31% increase over their winning bid in the 2024/25 winter, reflecting the aforementioned lack of supply growth in North American de-icing salt coupled with growing demand.

For a consumer and industrial salt price via Scotwood, we take Compass Minerals’ realized consumer and industrial pricing from 2025, subtract Atlas Salt’s expected cost per tonne at steady-state production and our estimate for incurred shipping and handling costs (Compass Minerals’ shipping and handling costs plus a 10% margin to third-parties), multiply this by 0.5 to reflect the splitting of profits between Scotwood and Atlas Salt, and then add back Atlas Salt’s operating costs.

On a 33/66% split to Atlas Salt’s production, our realized pricing estimate comes in at $89.06 CAD/tonne. This is very close to Atlas Salt’s posited ‘high case’ for realized salt pricing of $89.84 CAD/tonne and significantly higher than the UFS base case of $81.67. Our estimate is not precise, but if anything, it instills a great deal of confidence in the base case pricing applied to the UFS. Coupled with the stability of salt pricing over time (Figure 2), its persistent upward trend from structural supply shortages and the continuing uptick in prices in Atlas Salt’s markets, and we believe there is very little downside to the base case pricing utilized at $81.67. The Scotwood JV provides additional upside towards the $90.00 CAD/tonne range, pricing which we believe is feasibly realized given Scotwood’s geographic adjacency to Great Atlantic Salt, and the independence the JV provides them from large incumbents with tremendous negotiating leverage.

In the end, we have decided to use an identical starting salt price to the UFS to maintain consistency and conservatism, with the impacts of our estimated price shown in sensitivity analysis.

Other Miscellaneous Assumptions

Continuing on justifying our assumptions in Figure 11 from top to bottom, we now discuss the financing fees paid by Atlas Salt, annual G&A costs during the construction phase, and the discount rate used.

Atlas Salt requires significant financing packages for the construction of Great Atlantic Salt. Although the costs of construction are included in the UFS financial model, the costs of securing financing are not. In general, investment banking fees for a project of this kind are in the range of 5-7% of financing value. We have utilized 6% and applied it to our model in the same way we would a cost overrun on mine development capital expenditures.

The UFS model also omits the costs of being an incorporated entity and paying executives during the construction of Great Atlantic Salt. Based on recent historical years, ~$6M per annum appears to be a reasonable estimate, noting that the model is not particularly sensitive to this input.

For a discount rate, we have utilized an identical rate to the UFS at 8%. For reference, metals projects usually posit a rate of 8-10%, with potash projects using 5-8%. Infrastructure projects also utilize rates in the range of 5-8%. Given SALT’s bedded deposit style and infrastructure like pricing setting, we believe that potash and infrastructure rates are the best comparables. Because we believe in maintaining conservatism and want to generate high returns, we utilize 8%, the high end of potash and infrastructure projects and the low end of metals projects.

Operating Costs and Royalty

Vulcan Minerals maintains a fixed 3% royalty on all of Great Atlantic Salt’s gross revenues which can easily be accounted for. Other operating costs upon mine upstart are estimated in the UFS on a CAD/tonne basis, which we have duplicated exactly in Figure 11. Operating costs are then modelled to grow at a given inflation rate (2.0% in the UFS), while we model potential cost overruns using its own input.

Inflation Rates

The Great Atlantic Salt UFS has operating costs growing at 2% per year over project lifetime, while salt prices inflate at 4% per year prior to mine completion and 2% thereafter.

For our model, we have chosen an operating costs inflation rate of 3% per year. Although Canadian inflation levels have been in the range of 2% for the past year and would ideally hold in this locality, we are of the opinion that North American rates will adhere to a “higher for longer” trend in general in the coming decades as automation drives economic growth. In the specific case of Canada, the country has been in recession territory for the past twelve months, meaning a reversion from this trend is likely to drive inflation above current 2% levels. Selecting a 3% inflation rate reflects these perspectives and builds a more conservative model as compared to the UFS.

For salt pricing inflation, we have established that rock salt prices have continuously grown at an outsized pace relative to the broad economy (Figure 2), while never being subject to persistent downtrends due to the stability of demand and frozen supply. As is such, there is no reason to believe that rock salt inflation will materially deviate from historical levels (4.6% per annum on a 25 year timeframe) prior to Great Atlantic Salt being brought on stream, so we utilize the technical report’s 4% metric.

Once Great Atlantic Salt is brought online, annual output will reach 4.2 Mtpa at peak over a four year ramp up period. Concurrently with this development, New York’s Cayuga salt mine will have exhausted its reserves and have taken 2 Mtpa offline. This amounts to 2.2 Mtpa in incremental market supply from Great Atlantic Salt, which in the context of 36+ Mtpa in demand and ~10 Mtpa of high cost foreign imports does not seem like a significant or persistent catalyst impacting rock salt inflation from production upstart onwards. We could easily see rock salt inflation remaining in the range of 4% per annum over the 20 years post Great Atlantic Salt startup, and we believe it is difficult to build a case that rock salt pricing inflation be in the range of 2% as the UFS posits, especially if broad scale inflation is 3% as we propose. Thus, we select 3% in annual rock salt inflation as our production phase level, as this balances the persistence of the supply and demand imbalance in North American rock salt with the small incremental demand from Great Atlantic Salt, our “higher for longer” perspectives, and maintains a conservative outlook.

Overruns

Many mining projects reach production at higher capital and operating cost levels than anticipated. This is due to unforeseen events pertaining to mine geology, and, most frequently, metallurgical problems. Great Atlantic Salt is anticipated to cost $589.1M to develop, including contingency (overruns on unknown items) of $77.5M. The UFS states that operating costs may be within the range of -10%-+20% of the baseline estimates given, while capital costs (both development costs and maintenance capital) may fall within the range of -10%-+30% of baseline levels. Our overruns inputs simply add (or subtract for a negative value) whatever percentage we select to the baseline costs from the UFS. Note that the ‘capital costs overrun’ input impacts both development costs as well as maintenance capital.

For our base case, we have selected operating costs to overrun the UFS by 10%, while capital costs overrun by 15%. This is a significant failure on the part of estimating teams, however cost overruns are a frequent occurrence in mining which we would like to reflect in our model. Ultimately, these overruns are not easily foreseeable, but what we can confirm is that Atlas Salt is structurally lower risk from a cost overrun perspective relative to metals mines due to the bedded, low depth geology of the mine and the lack of metallurgical and processing engineering. We believe that a 20% operating cost and 30% capital cost overrun on Great Atlantic Salt, as the UFS poses as the high end of potential cost outcomes, would be a significant failure on a relative basis, and thus we choose 10% and 15% respectively to count overrun risk while also nothing that this is likely excessively punitive given the simplicity of the Great Atlantic Salt build.

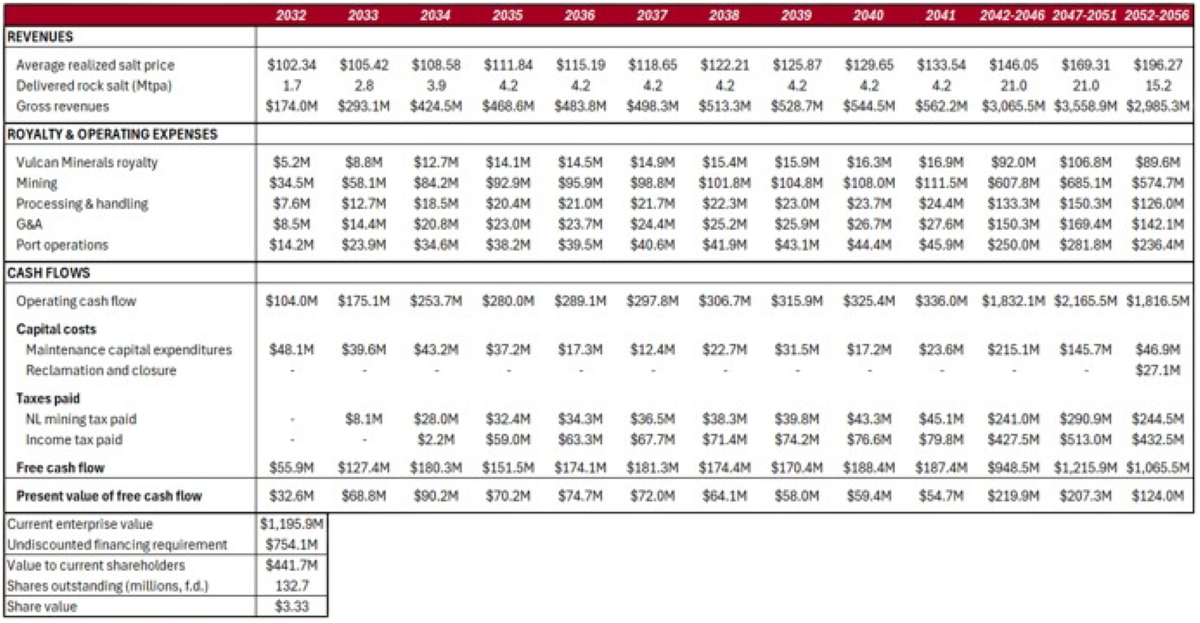

Great Atlantic Salt’s construction is expected to take four years in total. Although construction has already commenced we have forecast production to begin in seven years to allow for potential delays in construction and time spent securing financing. Figure 12 below shows our discounted cash flows model for Atlas Salt. Note that from 2042 to mine closure we have bucketed years to make our model more palatable, however cash flows have been both estimated and discounted on an annual basis to ensure accuracy.

Figure 12: Discounted Cash Flows Model

Source: Company Filings, Phi Research

Our annual salt production numbers are taken directly from the UFS and then multiplied by our estimated realized salt pricing levels to generate gross revenues. From there, Vulcan Minerals captures 3% of gross revenues, and operating costs are subtracted to infer operating cash flow. Capital costs follow the same pattern as in the UFS, only at levels 15% higher than the filings posit. Taxes are estimated as a percentage of operating cash flow using original UFS numbers. We have confidence in this estimation method as percentages are essentially constant across the production phase lifetime. From operating cash flow, capital costs and taxes can be subtracted to infer free cash flow, which can then be discounted to present and summed for an Atlas Salt enterprise value.

A large portion of this enterprise value belongs to future debt and equity holders, so we subtract SALT’s undiscounted financing requirement to arrive at a value belonging to current shareholders. Our undiscounted financing requirement is equal to the sum of all development costs (including contingencies and our forecasted overruns), G&A expenses from now until mine production begins, and fees associated with securing financing. Although these costs could be discounted, we utilize an undiscounted value as this accounts for the likely accrual of interest over the development timeline (discounting and interest accrual cancel directly over any period of time). Although certain readers may have a preference for modelling debt and equity requirements separately, estimating share price at financing, and subsequent per share dilution, we do not believe it is necessary and instead overcomplicates the model with an excessive number of low conviction assumptions (issuance price, issuance date, issuance size, etc.). Using our method, future equity being issued at current pricing equates to a neutral dilution impact. In all likelihood, large equity issuances come after large debt packages are secured, issuance prices are higher than current share prices, and actual dilution is lower than our model forecasts. It is very difficult to say if SALT shares will be worth two, three, or ten dollars in 12 months, so we utilize our method and omit this upside, while using capital cost overrun inputs to analyze the impact of potentially excessive spend and dilution.

Our model brings us to a current shareholder project NPV of $441.7M, which when divided across 132.7 million fully diluted shares brings us to an implied share value of $3.33. This represents a 115% premium to today’s close of $1.55.

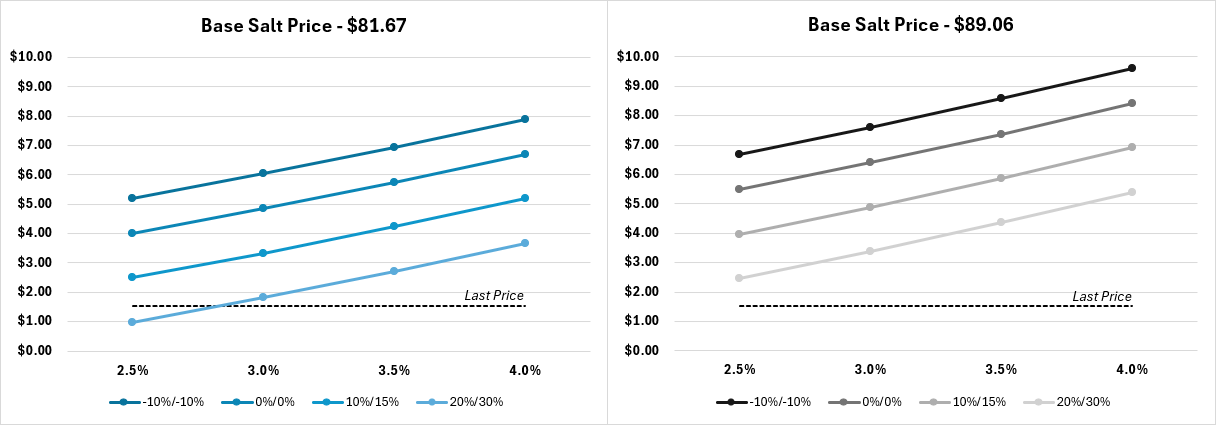

Sensitivity Analysis

To better understand the risk reward proposition provided by the Atlas Salt story and to assist in our final investment decision, we will analyze how our fair value estimate of share pricing is impacted by our model’s critical inputs. The most important factors in estimating fair value of Great Atlantic Salt to current shareholders are the baseline salt price used, the production level salt inflation level, and the operating cost and capital cost overrun level. Figure 13 shows a comprehensive analysis of these variables. The left hand side graph represents cases run at a base salt price of $81.67 CAD/tonne, the UFS model’s base case price, while the graph on the right hand side represents a base salt price of $89.06 CAD/tonne, equal to our estimate of realized price and in line with the high case analyzed in the UFS. The independent axis in each graph represents the post production salt inflation level used, while each dotted line represents a chosen operating cost/capital cost overrun level. Recall that the UFS proposed that operating/capital costs may vary from -10%/-10% of base level expectations up to +20%/+30%. The dashed line shown represents SALT’s last closing price.

Figure 13: Sensitivity Analysis

Source: Phi Research

Our sensitivity analysis demonstrates that SALT shares represent tremendous upside from current levels even when using conservative assumptions, meaning that an investment thesis does not rest upon the assumptions used, but simply whether or not the project is completed or not.

Project Financing

The completion of Great Atlantic Salt is contingent upon the receipt of significant debt and equity financing packages to fund development expenditures – this is the crux of realizing the share value we have demonstrated above. Below we will review the progress that has been made towards this objective and infer the likelihood of it being achieved.

The Great Atlantic Salt UFS was published in November of 2025, a critical step towards establishing the economics of the project via credible third-party, establishing a model and assumption set which financiers can stress test and use for decision making purposes.

For securing large debt financing (~$400M targeted), management has employed advisor Endeavour Financial, a London and Vancouver based mining advisor with over US$4B in debt financing raised for junior miners over the past ~20 years, as well as over US$28B in JV and M&A related financings. Thus far, Endeavour has secured multiple signed LOIs from potential financiers, including from export credit agencies, a positive signal for project cost of capital, government support, and project risk.

For equipment financing, SALT has partnered with Sandvik Mining and Rock Solutions, a prominent global mining equipment provider. In late 2024, prior to the publishing of the Great Atlantic Salt UFS, Sandvik and Atlas Salt entered an MOU for Altas Salt to employ three Sandvik continuous miners at Great Atlantic Salt, one roadheader, five 50-tonne battery-electric haul trucks, two battery-electric loaders, and one battery-powered bolter, amounting to $73M in equipment financing provided. In conjunction with providing equipment for the operation, Sandvik agreed to provide engineering and construction support through their proprietary software services, as well as equipment maintenance and other engineering consulting services. In February of this year, the details of the MOU were expanded to account for the increased mine output expectations under the UFS. Total equipment financing from Sandvik is now expected to be $132M, accounting for increased machinery needs, and representing nearly a quarter of Great Atlantic Salt’s development capital requirements. This is both a tremendous milestone for progressing towards securing complete project financing and also derisks Great Atlantic Salt in our eyes as a global expert in mining has willingly provided financing to support the upstart of operations.

On the equity side, management closed both an $8.7M offering in October of 2025, as well as a $15.2M bridge deal in June of this year, co-led by Raymond James and Ventum Financial. The $15.2M financing was initially announced at $10M but was upsized over 50% on strong demand. Notably, an unnamed strategic investor has made significant contributions on the equity side thus far, further derisking mine validity in our eyes as a party such as Scotwood or potentially current producing salt miners has made large commitments towards the success of Great Atlantic Salt.

As it stands, the only step that truly remains is converting the large construction debt LOIs into confirmed agreements, after which point the holes can feasibly be plugged with equity deals. We believe that the conversion of these agreements is significantly more likely than not: this is the driver of our investment decision in SALT shares. We can start from the fact that ~50% of mineral discoveries reach production, and then consider what Atlas Salt has at this point that a typical discovery would not. Unlike metals and potash projects, there is a very strong business case to be made around Great Atlantic Salt, its competitive standing, and the unfulfilled need which its output will satiate. At the same time, rock salt prices are steady and increasing, eliminating commodity risk from a creditor’s perspective. Great Atlantic Salt is a bedded deposit, has inherently low risk geology, and a very simple construction plan with no metallurgical requirements. The project has completed its Environmental Assessment (in essentially record time, signaling strong government support), has First Nations support, and has faced no backlash from NGO’s. Great Atlantic Salt has already begun initial construction works, has secured machinery financing and engineering consultation from a highly credible global leader in the space, and is also in an optimal geographic location for securing skilled labour, low cost power, and easy access to port and highway infrastructure. From a creditor's point of view, nothing is missing. This project is a layup in comparison to other mining projects; it is only a question of what a reasonable financing rate is. The process of finalizing agreements typically takes 12-24 months, with just under 8 months having passed since the publishing of the UFS.

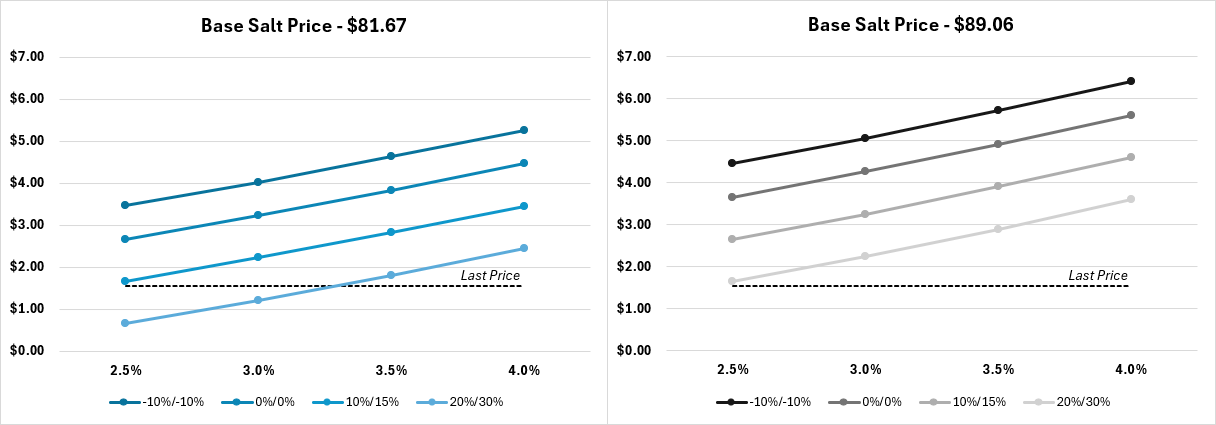

Given the above, if we had to assign a probability to the likelihood of Atlas Salt converting debt financing LOIs to guaranteed deals, we would have to say that it is significantly higher than the ~50% baseline for an average mineral discovery. Given this information and our sensitivity analysis in Figure 13, shares are clearly underpriced on an expected value basis. Figure 14 shows our sensitivity analysis assuming a 2/3 chance that financing is secured, with a 1/3 chance assigned to a scenario where shares are completely worthless.

Figure 14: Sensitivity Analysis – Expected Value of Shares at 2/3 Success Rate

Source: Phi Research

Summary and Investment Decision

As previously stated, an investment thesis on Atlas Salt boils down to two things: whether financing is secured, and whether or not mine construction goes smoothly. If yes to both, tremendous gains are inevitable. If no to both, then shares will perform very poorly. This is somewhat of a binary setup, but what we believe we have established in writing this report is that a 1 is far more likely than a 0 in the case of Great Atlantic Salt. For every measurable reason construction and operational risks are low on a relative basis, the commodity pricing environment is structurally positive for the long term, and project validity has been well delineated by credible third-parties like Sandvik. The risks are significant, but with a probability of well over 50% we can see SALT shares being worth multiples of their current market value in the near term. Strong Buy.