Auxly Cannabis Group Inc. (TSX: XLY), After the Weeds Clear

Published on 2026-05-28

Auxly Cannabis Group Inc. is a Canadian producer of cannabis products, specifically dried flower, pre-rolls, and cannabis vapes. In the wake of the overwhelming cannabis investment bubble which came with the legalization of the drug in Canada and subsequent withdrawal of capital from the space, the company trades at a level which we see as deeply undervalued given the quality and durability of the business model. In relevant metrics, Auxly is both the highest quality and most attractively valued company in the growing global cannabis market, and we anticipate it to generate strong returns in the long term in spite of current negative sentiments.

Auxly’s cannabis growing facility is located in the “Tomato Capital of Canada”, Leamington Ontario, sitting on the shores of Lake Eerie at a latitude in line with that of Northern California. The town has historically been a hub for the growth of a variety of vegetables including tomatoes, cucumbers, and peppers, and exists as a natural fit for cannabis greenhouse operations for a number of reasons. The temperate lakeside climate and high levels of sunshine offer a low cost basis for both climate control and supplemental lighting in indoor facilities. In addition, Leamington offers multiple generations of skilled greenhouse workers, as well as convenient access to large markets like Toronto. Unlike a number of surrounding cannabis operations in the area who have retrofit existing greenhouses, Auxly’s facility has been purpose built for cannabis cultivation and features a high degree of automation, sits on owned land, and utilizes on site power generation. The result of the above is the firm operating at a globally competitive cost basis, with only two other facilities in Canada producing at a comparable scale or technological level.

The Leamington facility grows over 150 unique cultivars, which once harvested are processed and prepared for sale either on site or at Auxly’s Charlottetown facility. The Leamington facility handles the completion of both dried flower and pre-roll products, which are then sold to third party retailers for consumer purchase. Auxly’s relationship with Imperial Brands (~20% shareholder of XLY and top five largest tobacco company globally) has allowed the company to successfully implement advanced high-speed pre-roll technology, further strengthening their cost position relative to peers.

Figure 1: Leamington Pre-Roll Operation

Source: Company Presentation

Auxly’s non-flower products, namely cannabis vapes, are designed and manufactured at Auxly Charlottetown. As compared to the dried flower market, the cannabis vapes market has significantly higher barriers to entry as a result of technological requirements. As compared to peers who purchase vape hardware and tooling premade from third parties, Auxly has vape hardware custom made to ensure that it is consistently functional with their cannabis oils. This allows XLY to maintain the lowest product failure rate in the vapes space, which when bundled with their cumulative R&D represents a good competitive advantage. Once vapes are manufactured, similar to flower and pre-rolls, they are sold to retailers who then distribute products to end consumers.

The Cannabis Market Over Time and Competitive Dynamics

Cannabis was made legal in Canada in late 2018, with the event being surrounded by an effervescent and misguided surge of financing into both public and private Canadian cannabis projects. Cannabis companies raised over $3.5B in 2017, followed by an additional ~$13.8B in 2018. What followed was a severe overbuilding of the Canadian cannabis industry and a vicious competitive environment. Cannabis investments were quickly rendered “dead money”, leaving a long lasting sour taste in the mouth of investors which upholds persistent negative sentiments to this day. Figure 2 shows the performance of an index of Canadian cannabis companies from legalization to date (constituents: TSX-OGI, TSX-WEED, TSX-ACB, and TSX-XLY). Note that constituents are only made up of large surviving entities, not failed marginal peers.

Figure 2: Canadian Cannabis Company Share Performance

Source: S&P Capital IQ, Phi Research

Ongoing Producer Exits

After nearly ten years of legal cannabis sales and the widespread withdrawal of financing, the market has become subject to participant exits.

Canadian producers are required by law to pay an excise tax of $1.00/gram (or 10% of wholesale selling price if that is higher than $1.00/gram), a policy which was designed at legalization under the assumption that prices would be in the range of ~$10.00/gram. Post legalization, prices rapidly collapsed (~$1.00-2.00/gram at present) and many producers were forced to charge prices below excise tax levels, leading to significant delinquent tax accounts which the CRA still pursues at present. Many small producers have been subject to liquidation in order to settle these debts, a trend which the CRA cites as continuing.

Irrespective of tax delinquencies, a number of cannabis companies have been forced to exit the market as a function of both time and lack of financing. Even after nearly a decade of operations, many cannabis companies have not been able to realize positive cash flows, an operational status which does not last in a dry financing environment.

Current Demand Setting and Competitive Environment

As a result of ongoing producer exits and the degradation of the illicit market, the competitive environment in cannabis has stabilized significantly from late 2023 onward. During historic periods of oversupply, inventory levels and available growing space have exceeded demand requirements greatly. Figure 3 shows the decreasing licensed indoor growing area in Canada, the falling fraction of cannabis which spoils in storage, as well as relatively flat wholesale inventory levels from 2020 to present. The evolution of these metrics over time is a function of ongoing producer exits and demonstrates the improvement in supply trends up to the present.

Figure 3: Supply-Side Trends

Source: StatsCan, Phi Research

In addition to improving supply-side trends, the Canadian cannabis market continues to grow from the demand side. As per StatsCan data, cannabis sales rose 6.1% year-over-year last year and have increased by over 37% compared to three years earlier.

Although the historical evolution and positive momentum in both the supply and demand spaces is encouraging, what is important to evaluate from an investment perspective is how things will unfold on a go forward basis. In the demand space, over 20% of Canadian cannabis sales are still captured by the illicit market, a share which shrinks on a yearly basis. In the supply space, many producers remain in negative cash flow or extremely low margin positions, despite the stability of demand and lack of investment in the space. This signals further market exits going forward and a stronger competitive standing for remaining entities. From both a supply and demand perspective, it appears that there are structural tailwinds which will drive XLY’s revenues higher for the foreseeable future, and once market share capture from both peers and the illicit market dissipate, Canadian cannabis will exist as a consumer staple market similar to alcohol, growing roughly in line with GDP.

Margin Position and Durability of Competitive Standing

As previously mentioned, the vast majority of both public and private cannabis producers operate extremely low margin businesses, with only Auxly and four other peers globally operating at sustainable profitability levels (Nasdaq: VFF, TSX: CURA, CNSX: TRUL, and CNSX: GTII, bottom of Figure 4 peer group). Figure 4 shows a group of global cannabis operators with an emphasis on those who market dried flower, pre-rolls, and vapes to third party retailers. Certain peers have been excluded who have an excessive amount of retail sales exposure, as we view this as a fundamentally different business than that in which XLY operates.

Figure 4: Global Cannabis Peer Group

Source: S&P Capital IQ, Bloomberg, Phi Research

What is clearly visible from Figure 4 is Auxly’s standing as a cost leader in the industry. This is in part due to management’s discipline, but is mostly attributable to their asset base. Auxly Leamington is a legitimately state-of-the-art facility; the scale and efficiency of the operation can only be matched by a few similar operators. At present, marginal competitors do not have the ability to lower prices given negative to low single digit margins. Going forward, it seems extremely unlikely that new financing enter the space in order to construct a facility which competes with Auxly Leamington on a cost basis given the proximity of the market to maturity, the ~3 year construction time to bring production online, and the current lack of capitalization in the space. As is such, we believe Auxly’s competitive advantage is durable and structural, and from a competitive standing and market evolution perspective the shares should offer an attractive investment contingent upon valuation.

Global Growth Prospects

Although not central to our investment thesis, the potential for growth in the global cannabis market, and Auxly’s potential participation in such growth by way of their relationship with Imperial Brands, could potentially offer material upside to XLY shares. Figure 5 shows the current legal status of cannabis globally. Note that Canada is the only G7 nation with a legal recreational cannabis market at present.

Figure 5: Legal Status of Cannabis Globally

Source: Company Presentation

Although cannabis is not fully legal from a recreational perspective in many global markets, a number of major markets are currently in the process of loosening regulation or rolling out recreational usage. In Germany, cannabis was legalized recreationally in 2024, although at present at home growing and “cannabis clubs” are the only form of legal supply. A retail pilot project has begun which is anticipated to be slowly rolled out in the coming years into a legitimate recreational cannabis market. In the United Kingdom, medical marijuana was made legal in 2018, with public opinion steadily progressing towards the desire for legal recreational use. Although legitimate progress in the recreational market is limited, XLY has shipped small test volumes to the U.K. medical market through Imperial Brands in order to gauge potential interest. The United States remains a patchwork of regulation, with 25 states allowing recreational cannabis and the drug remaining illegal on a federal level. In April of this year, the Department of Justice rescheduled state-licensed medical marijuana, as well as mandated the Drug Enforcement Administration to formally consider the rescheduling of all cannabis under the Controlled Substances Act (link). Although this does not constitute legalization or a future guarantee of such, these are material steps towards the opening of what would be the world’s largest market. In Australia, medical marijuana is legal nationally, with recreational use being legal under limited possession laws and home growing only in the Australian Capital Territory.

There is no major market in which it is currently a guarantee that retail recreational cannabis sales present an immediate opportunity for XLY, but across the globe there are a number of opportunities which appear to be moving in the correct direction. Canada is currently the largest exporter of cannabis globally due to the infrastructure established during the 2018 investment boom, and firms like Auxly hold valuable intellectual property and knowledge on the operation of large scale growing operations. In spite of export costs, Auxly Leamington is able to produce cannabis at a globally competitive rate due to scale, favourable climate, and power access. In addition, Auxly’s partnership with Imperial Brands establishes important connections for global distribution. Altogether, the company is well positioned to be a significant beneficiary of global demand expansion given their product quality, cost of production, and global relationships via Imperial Brands as a strategic holder.

Although under normal industry conditions potential growth in global demand would be viewed as an unequivocal positive, the prospect of scope expansion may be frightening to investors in the cannabis space. Capital discipline has clearly been lacking historically, however we do not believe this will be the case for XLY going forward. In January of this year, public competitor Ayurcann filed for creditor protections largely as a result of ~$10.6M in unpaid excise taxes, resulting in a court-ordered sale process of the firm’s assets. Auxly participated in the bidding process but ultimately did not generate the highest offer and did not submit a secondary bid. We view this as a legitimate signal of capital discipline, as any firm participating in ‘empire building’ activities would have likely pursued the acquisition at disappointing return rates. Management has indicated verbally that they have no intention of pursuing low margin or low IRR opportunities, and we tend to believe them given the above and their incentives plans which are laid out below.

Corporate Governance and Management Alignment with Shareholders

XLY is led by Hugo Alves, former Senior Partner at Bennet Jones LLP. Alves completed his JD in 1999 at the University of Toronto and is the company’s largest shareholder excluding Imperial Brands. Insiders are by far the largest shareholder’s of the company as a whole, having bought over 310 million net shares since 2020 with a total of zero sold. This is supplemental to stock-based compensation, which accounts for the largest portion of executive compensation.

Auxly’s board is chaired by Genevieve Young, current President and COO at consultancy firm Global Public Affairs, employing over 75 consultants in the space. Young holds an MBA from Queen’s University and is also a member of the board for the Canadian Pharmacists Association and the Society of Obstetricians and Gynecologists of Canada. Other members are Vikram Bawa, Chief Marketing Officer of Bosch Home Appliances and a previous senior marketing executive for both Terrene Ltd. and Logitech, Conrad Tate, previous Director of Corporate Development for Imperial Brands, Hugo Alves, current President and Chief Executive Officer of Auxly, and Troy Grant, former Director of Coporate Finance for Citadel Securities and current Director for Alcora Advanced Materials and Birchtech Corp.. The board has a total of five members of which four are independent. Although this may be a small board on a general scale, it is appropriately sized on a relative scale given Auxly’s ~$200M enterprise value, and independence is high in spite of limited membership. Independent directors receive ~60-65% of their compensation in the form of RSU’s and share awards, with the rest coming in the form of a cash retainer. Note that board members retain the optionality to receive cash retainers in share form, of which ~50% of such was accepted in share form in 2025, pushing total share-based compensation to ~75-80% of total compensation.

In addition to Hugo Alves, the remainder of Auxly’s management team is capable and well qualified. Chief Executive Officer Travis Wong stepped into his role in 2023, following previous roles in investment banking with Nomura and as a Senior Associate with KPMG. Wong is a CPA charter holder and has completed an MBA at Oxford University. Andrew MacMillan, Senior Vice President, Commercial is the former Chief Executive Officer of PEI Liquor and has previously served on the board of Inner Spirit Holdings, bringing relevant cannabis and government distribution experience with him to XLY. Michael Lickver, Auxly’s President and right hand man to Alves, holds both his JD and MBA from Western University, previously co-founded the Cannabis Group at Bennett Jones LLP, and is a current Adjunct Professor at Western University. Executive compensation is composed of an annual base salary, annual incentive plan, and share-based awards. Alves, Wong, and Lickver all received ~40-55% of 2025 annual compensation in share-based awards, primarily as RSU’s with a three year vesting period. We like the balance in compensation between short and long-term incentives, the strong insider ownership, and management’s inability to hedge equity positions. Over the last two years, annual incentive plan compensation has increased for executives materially as a result of the company being pulled out of potential bankruptcy, the growth of revenue by ~60%, and the step change in EBITDA from deeply negative to near 30% margins. Although this is indeed cause for bonuses being paid, we will periodically monitor the situation to ensure that bonuses do not reach an excessive level or continue growing out of line with financial execution.

In general, XLY’s corporate governance scene is positive. Share-based awards are the central piece aligning management and board members with the shareholder base, no hedging policies maintain the validity of the structure, and in spite of 40%+ of compensation stemming from long-dated RSU’s and common equity, insiders continue to buy aggressively in the public market with spare capital. Both the board and management team appear to be impressively qualified, especially given Auxly’s size and consensus market perception of cannabis investments at present.

Valuation

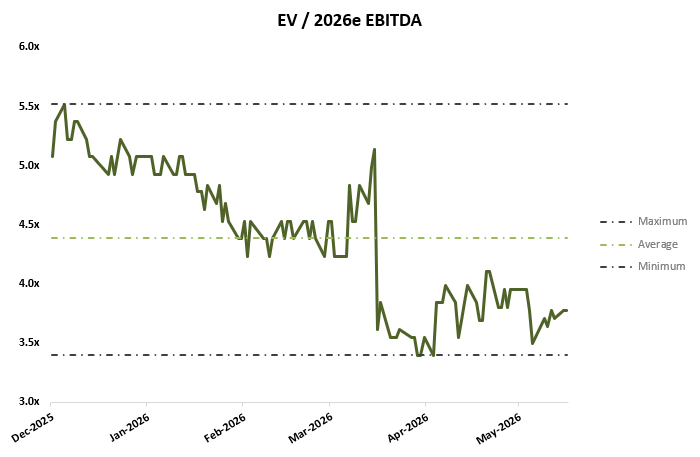

Auxly currently trades at ~3.6x EV/NTM EBITDA and ~4.2x EV/TTM EBITDA. Note that since broker coverage was reinitiated in December of 2025 EBITDA estimates for 2026 have increased over 8% which instills some confidence in the execution of these targets. Figure 4 (above) shows XLY compared to its peers in the global cannabis space. Note that Auxly is the lowest valued peer on an EV/EBITDA basis, in spite of being the only firm to withhold margins over 20% and positive y/y EBITDA growth (64%). Figure 6 (below) shows XLY’s relative valuation since analyst coverage was reinitiated in December of last year.

Figure 6: Relative Valuation

Source: Bloomberg, Phi Research

Shares are clearly inexpensive on an EBITDA basis. For the full year 2025, we calculate free cash flow to the firm of $26.7M, which equates to an 11.0% firm free cash flow yield. Excluding a one-time accounts payable movement of $9.1M, rearward-looking free cash flow yield would sit at 14.7%, an extremely high level especially for a growing consumer staple.

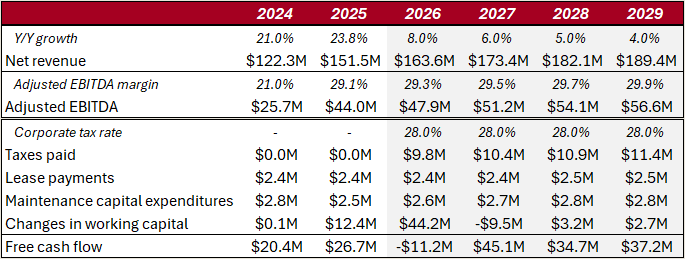

For a comprehensive analysis, we forecast free cash flow on a go forward basis and associated financial metrics. Figure 7 shows XLY’s recent annual financial performance and our expectations from 2026 to 2029. Revenue has grown at over 20% in 2024 and 2025 as a function of competitor exits and the diminishing illicit market, as well as excellent product branding and innovations on the part of XLY management. In Q1/2026, Auxly’s share in the Canadian market reached ~7% as compared to ~6% the year prior. We forecast growth in net revenue in the mid-high single digits range in 2026 and 2027 and in the mid-low single digits range beyond that point. From 2025-2029, we see revenue increasing ~25%, a result of continuing capture of the illicit market (recall the illicit market is ~20% of sales at present, a full capture would be a 25% increase in legal market size) and additional competitor exits which will allow for an additional few percentage points of market share capture. We forecast EBITDA margins to expand ~80 bps by 2029, which we see as a very conservative estimate given the high fixed cost structure of XLY’s operations and future growth in net revenues. Note that both our revenue and EBITDA estimates are roughly in-line to below published sell-side analyst estimates at present.

In spite of the likelihood that Auxly is able to employ previous tax losses strategically going forward, we apply a 28% corporate tax rate on EBT to forecast cash taxes paid. Predetermined lease obligations have been disclosed for both 2026 and 2027 at ~$2.4M. For 2028 onwards, we forecast leases to grow at the pace of inflation, as well as maintenance capital expenditures from 2026 onwards.

The trickiest part of our free cash flow forecasting process relates to changes in working capital, specifically regarding accounts payable. As previously alluded to, Auxly’s accounts payable swung quite violently in 2025 and have historically done so across the Canadian cannabis industry due to inconsistencies in excise tax payment terms, historically unstable cash flows, harvesting cycles, an industry standard of long payment terms, and other factors associated with the maturation of the market. Management has published committed accounts payable releases for the following four years, of which there are none except for in the remainder of 2026 ($39.9M release, or the entirety of accounts payable on the balance sheet at present). This accounts for a significant working capital build and actually forces free cash flow negative for the balance of the year (XLY does have sufficient capital resources through cash on hand and undrawn debt to finance the event, net debt to adjusted EBITDA is currently 0.05x). Beyond 2026, we have forecast payables to sit at ~8% of net revenue, a very conservative estimate. Nonetheless, this implies a working capital release of $9.5M in 2027, after which point changes stabilize. Operating assets are forecast as a percentage of revenue, in line with historically stable levels.

Figure 7: Financial Estimates

Source: Company Filings, Phi Research

Although inconsistently due to the impacts of working capital, free cash flow is expected to rise materially in the coming years as a result of top-line growth and modest margin expansions from the previously discussed supply and demand dynamics in the market. Note that our forecasts give no credit to the potential for international expansion, events which could potentially provide material upside to our estimates.

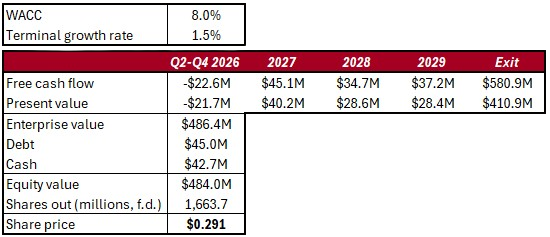

For our discounted cash flows analysis (Figure 8), we discount our free cash flow estimates to the present, noting that free cash flow produced in Q1/2026 is already included in net debt and is thus excluded from the remainder of this year’s cash flows. In addition, we use half-year discount factors to account for today’s date.

For an exit value, we utilize a growing perpetuity under the assumption that the Canadian cannabis industry will be relatively mature by the end of the decade. This is a reasonable assumption given the relatively small remaining share of the illicit market sales (~20%), the lack of barriers for consumers to purchase the products at present, and the lack of public pushback on legalization as a whole. For reference, alcohol markets took ~20 years to reach a mature state post prohibition, while if Canadian cannabis reaches maturity in 2030 this would be ~12 years post legalization. Post prohibition alcohol markets faced challenges in reaching maturity due to alcohol infrastructure taking years to rebuild from the lack of financing in the great depression era, significant disruptions to infrastructure builds and barley/feedstock supplies due to WWII, aged spirits taking many years to produce, national regulation remaining fragmented, and the pushback from NGO’s with strong influence. None of these headwinds apply to Canadian cannabis: the industry was overbuilt from legalization onward, feedstock markets are secure and consistent, cannabis can be grown and produced quickly, national regulation is essentially homogenous in Canada, and there is little credible public pushback at this point. Because of this, we see it as reasonable that cannabis achieve a state of ‘mature consumer staple’ within the next five years, and thus model it as such in our cash flows analysis.

Figure 8: Discounted Cash Flows Model

Source: Phi Research

In our base case, we utilize a perpetual growth rate of 1.5% (below GDP standard of ~2%) and a WACC of 8%, bringing us to an implied share value of $0.291, 100.6% higher than today’s close of $0.145.

Determining an appropriate cost of capital for XLY requires a fair amount of discretion as a result of a number of factors. Prior to 2023, XLY shares were subject to a great deal of volatility as a result of the cannabis investment bubble and harsh market conditions, which makes the utilization of a five year beta to estimate cost of equity impractical. For the entirety of 2023, shares bounced around in the range of $0.02 and $0.03 with very little liquidity, and from 2024 onwards XLY has actually demonstrated a negative correlation to broad market returns. Unfortunately, other Canadian public cannabis companies can not be analyzed to infer the sensitivity of the cannabis market to broad economic movements as a result of similar situations to the above being observed across all equities. Instead, we must infer the sensitivity of cannabis to macroeconomic events using indirect inference. At maturity, we believe that changes in consumer cannabis spending will likely resemble those seen in alcohol. Alcohol spending habits are notoriously stable across macroeconomic regimes primarily because alcohol is a part of strongly formed habits and is an affordable luxury. As a result, when economic downturns come alcohol consumption usually remains relatively stable (sometimes even increases), making companies like Pernod Ricard, Heineken, Diageo, and Constellation Brands notoriously defensive stocks. Beta levels range from ~0.3-0.7, implying costs of equity in the range of ~4.5-6.5% at current Canadian interest rates.

From the consumer’s perspective, we believe marijuana takes a very similar place in spending habits as alcohol does; it is an inexpensive, highly habitual indulgence. It is often a consistent part of a given consumer’s day and one of the last pieces of spending to be cut when difficult financial times present themselves. As a result, Canadian cannabis long term beta levels should resemble those seen in the alcoholic beverages space, and costs of equity should be in the range of ~5-7%. This corresponds well with Auxly’s current cost of debt of 6%, as equity financing rates should be slightly higher than appopriately priced debt. Because Auxly has very low debt levels at present we do not calculate WAAC on a deconsolidated basis, and simply apply an 8% cost of capital to cash flows, a level that is above the high end of those seen in the alcohol industry. This preserves the conservative nature of our analysis and also accounts for the added liquidity risk in an equity like XLY as compared to large alcohol brands.

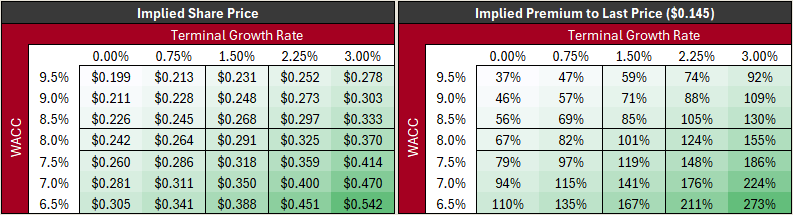

For the sake of rigour, we have conducted a sensitivity analysis on our discounted cash flows model, analyzing the impact of changes in WACC and terminal growth rate on implied share value. These inputs have significant effects on the exit value used in our analysis, and thus are the strongest determinants of current fair value. Note that XLY shares most recently traded at $0.145.

Figure 9: Sensitivity Analysis

Source: Phi Research

Even at a punitive cost of capital of 9.5% and assuming zero growth in revenues beyond 2030, shares are undervalued significantly and are poised to deliver strong returns.

Summary and Investment Decision

Auxly exists in a growing Canadian cannabis market where competitive pressures are no longer expanding but are instead continuously diminishing. The company sustains best-in-class margins as is and produces high amounts of cash on a relative basis. Auxly is poised to continue capturing market share in an overall growing space for years to come and has the asset base, management team, and incentives in place to ensure the highest likelihood of doing so. Although current sentiments are muted and the story may move slowly at times, Auxly is a structural beneficiary of the evolving supply and demand environment in Canadian cannabis and a clear expected outperformer on a ten-year basis. Strong Buy.