Circle Internet Group, Inc. (NYSE: CRCL), The Digital Dollar Opportunity

Published on 2026-03-10

Circle Internet Group (NYSE: CRCL) is an international issuer of stablecoins; the only functional form of digital cash. The company is poised for a persistent period of staggering growth in stablecoin adoption and subsequent financial performance which we believe is not fully reflected in CRCL share prices. For investors, CRCL represents a unique opportunity to invest in an undervalued, rapidly growing, and countercyclical asset which we believe far exceeds the threshold of being worthwhile.

Circle’s product offerings are not in the traditional sense of the word “cryptocurrency”. The firm issues stablecoin’s like USDC (US dollar stablecoin) and EURC (euro denominated stablecoin) by way of decentralized exchanges and purchases legitimate fiat dollars for a 1:1 backing on issued tokens which can be immediately redeemed for fiat dollars. Circle earns interest on the liquid assets it holds and generates cash flow through this channel almost exclusively. As long time skeptics of the decentralized finance system, it has been enlightening to learn that something like stablecoins exist and have served a legitimate purpose which can easily be dismissed as “crypto garbage” or the like. In this report we will provide an overview of the past, present, and the future of the decentralized financial system to provide context on the role of stablecoins in an evolving global economy. Throughout we will discuss competitive dynamics, regulatory environments, traditional cryptocurrencies, and most importantly; why stablecoins are a value-add offering and why their reach will expand significantly in the future.

The History of Stablecoins

In October of 2008, the pseudonymous Satoshi Nakamoto published the white paper “Bitcoin: A Peer-to-Peer Electronic Cash System". Bitcoin was pitched as a form of digital cash which was secure and digitally transferable, all operating on a communal ledger known as a “blockchain”.

Figure 1: The Bitcoin White Paper

Source: Bitcoin.org

The first ever cryptocurrency was set to have a fixed supply from now until eternity and with the proper function of the blockchain, which provides bitcoin as incentives to its operators semi-probabilistically, the entire system could function without a trusted intermediary like a bank (for a stronger understanding of blockchain systems, see (link)). It was and still is in the truest sense of the word “decentralized”. There is no CEO, there are no headquarters, and there is no possible way of modifying the operation of the BTC system without a broad consensus amongst millions of market participants. Bitcoin is not “ran” by an individual or company, it is an open source ecosystem that exists in the cumulative cyberspace. You can not call somebody from Bitcoin, you can not physically see or approach it, and no fist, baseball bat, or drone strike can eliminate or modify it. It is untouchable.

In the modern world, 18 years after the Bitcoin white paper was published, this ‘untouchability’ is what gives BTC value. Although it may not be inherently valuable to you or I, and in spite of the amount of speculative trading surrounding Bitcoin and other cryptocurrencies, there does exist a large demand for BTC as a decentralized asset, somewhat akin to the financial demand for gold and the growing financial demand for other metals. Determining the size of this legitimate market is somewhat tricky (this is why we stick to buying stocks), but Bitcoin exists as a legitimate store of value, and all signs point towards that it always will.

Although Bitcoin has essentially created what is now a multi-trillion dollar market for a decentralized asset while also sparking the creation of thousands or even millions of inferior imitators, it has ultimately failed at its original goal; creating an electronic cash system. As previously alluded to, Bitcoin’s aggregate market size and coin prices are highly unpredictable and notoriously volatile. Although the argument could be made that prices will stabilize with time and institutional “price discovery”, 18 years after founding the situation has not improved. Ultimately, for those seeking a digital cash system it is not worth waiting around to see what happens with Bitcoin because a better system began to emerge is 2014; stablecoins. Bitcoin and most other cryptocurrency’s values are determined by an algorithmic supply and market demand, Tether USD (USDT) sought to create a coin which was instead directly tied to the value of the US dollar. The successful creation of such a coin would allow cryptocurrency investors trading on decentralized exchanges to essentially hold USD, a stable asset, in between crypto trades rather than being forced to move money on to and off of decentralized exchanges so frequently. Tether USD emerged making the claim that for every USDT coin issued, $1.00 in USD was held in their bank accounts. The idea quickly gained momentum and became the enabler of crypto trading worldwide.

In 2016 and 2017, Bitcoin realized gains of approximately 3,000%, pushing cryptocurrency towards the mainstream and skyrocketing demand for USDT. What regulators realized at this time was that cryptocurrency as a whole needed to be addressed in some way, but how or what exactly to do remained unclear. In spite of this, certainly realities emerged, namely the previously discussed fact that the decentralized system did not need permission to exist and that any attempt to get rid of it, whether financial efforts or even military, would be a waist of time. In a way the situation could draw a comparison to legal drugs and alcohol; you can’t stop people from getting high, so you might as well draw a perimeter around the activities and collect some tax revenue. Two of the most pressing issues for drawing a perimeter around the decentralized system was the analysis of liquidity or the robustness of the system in the case of a market fallout, and the uniqueness of the decentralized system from the banking system (i.e., nobody operating as a bank outside of regulatory scrutiny). USDT quickly fell under the eyes of the law as a “liquidity provider” in the space as well as due to the similarities drawn between their offering and bank deposits. Although Bitcoin’s novel nature was difficult to make heads or tails of, the niche that USDT served had tangible and easily observable risks; a stablecoin losing its peg could be a catastrophic ‘bank-run’ like event with cascading effects across crypto markets worldwide. If traders required liquidity in USDT and it was not available, panic would spread and a ‘crypto depression’ would ensue. Clearly this was the low-hanging fruit from a regulatory perspective and the easiest place to start; it was vital to regulators that USDT held the cash reserves it claimed to hold and that the entirety of their supply was actually redeemable for USD to traders. What regulators found was that this was not likely the case.

Tether did not historically offer audit information nor proof of reserves to regulators, and given the risks surrounding anything crypto related at the time, many were suspicious that Tether had access to traditional banking services at all. In 2018 Tether’s parent company Bitfinex, a decentralized exchange company, lost access to US$850 million after the funds were seized by foreign authorities. To plug the holes, Bitfinex borrowed the $850 million from Tether’s USD reserves which proved beyond a reasonable doubt that Tether’s reserves were at least temporarily not backed 1:1 with cash. Tether fell under investigation by the New York Attorney General in 2019 for misrepresenting its reserves to the public, with proof emerging that the company had less than three quarters of USDT value held in cash at given times. Additionally, much of what was touted as “cash” reserves was instead money market funds and even corporate bonds. Tether settled for an $18.5 million fine, was barred from operating in New York, and was mandated to provide quarterly reserves updates (holding exclusively cash at 1:1).

With this sequence the regulatory fence had been partially built, but from a business case perspective a new opportunity emerged. Historically competing with Tether would have been virtually impossible: stablecoins are somewhat of a natural monopoly/oligopoly due to network effects and the game-theoretical principle of coordination. In spite of this, a firm who worked with regulators cooperatively and had a strong reputation with traders as being reliable could now swoop in and capture a large portion of market share while also addressing unserved markets. Circle Internet Group launched in 2018 and began to address this need with a high degree of success. The company launched USDC, a 1:1 US dollar backed stablecoin with a compliance-first mindset, regulated reserves, and monthly attestations. With the Circle value set, USDC grew from ~$462M in circulation to ~$42B from 2019 to 2021, capturing demand from customers who wanted their stablecoin to be just that: stable.

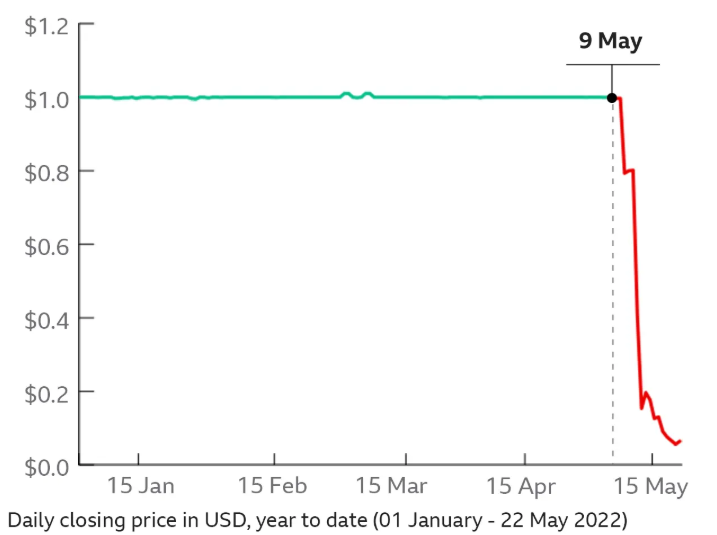

Global stablecoin demand erupted in the years that followed, with a multitude of new peers entering the market and now serving hundreds of billions of dollars in coin demand. Stablecoins began emerging not only as liquidity for crypto markets but as a source of remittance payments, decentralized cross-border transfers, and as a means of international operators to gain exposure to the US dollar. Around this time emerged the idea of the algorithmic stablecoin, a stablecoin that remained pegged to USD value not based on cash reserves but using other cryptocurrencies as collateral and operating a trading algorithm with such reserves to keep the value at 1:1. Although this may seem like a ridiculous idea to reasonable people, algorithmic stablecoins garnered a significant amount of popularity as they were truly decentralized, an accolade which USD backed coins could not boast. This alone allowed them to capture a portion of demand from fiat-backed peers like Circle. In spite of this value proposition, the idea failed before regulators could even begin to ponder how to address the situation, with one of the largest algorithmic US dollar stablecoins, TerraUSD, collapsing in 2022.

Figure 2: The Collapse of TerraUSD

Source: BBC

The fall marked a loss of $40B in value and served as somewhat of a “Lehman Moment” for the crypto world. It was clear that regulators had to become more diligent and draw a stronger perimeter. All algorithmic coins lost validity in the fallout of TerraUSD losing its peg, regulatory scrutiny intensified, and within a year what was left was Tether and Circle holding roughly 90% of market share.

In spite of the oligopoly at hand, regulators had work to do. As previously discussed, eliminating stablecoins or cryptocurrencies completely is not a feasible option. Even if it were, the reality is that United States regulators actually have strong incentives to increase the breadth of stablecoin reach. Higher demand for USDC means higher demand for the greenback, and it means demand which in the absence of the defi system could not have been satiated. Higher demand for US dollars means cheaper financing for the US government (more government spending potential), lower costs of financing in US capital markets (higher corporate investment and economic prosperity), and a growing USD dominance position that stymies any Chinese, Russian, or other adversary’s economic leverage. In the context of potentially trillions of dollars of USD demand which would otherwise not be fulfilled, the impact on American prosperity is very real and is thus worth fighting for.

In July of 2025, two years after the collapse of TerraUSD and the consolidation of the stablecoin market, US lawmakers signed into effect the Guiding and Establishing National Innovation for U.S. Stablecoins Act (GENIUS Act), with Circle making its initial public offering right around the same time. The GENIUS Act is the first ever U.S. federal law specifically regulating stablecoins, with the US joining a slew of other major economies in officially regulating and permitting the issuance of stablecoins (examples include the United Kingdom, Canada, Singapore, Japan, the UAE, Switzerland, Hong Kong, and the European Union).

Figure 3: Signing of the GENIUS Act

Source: CNBC

The GENIUS Act legalizes and establishes stablecoins as a financial product, essentially crystalizing the precedent set in the 2019 Tether investigation. The act establishes that 1) stablecoins have a 1:1 backing in highly liquid USD securities like dollars or short term treasury bills at all times, 2) issuers must publish monthly reserves disclosures, 3) only licensed participants are permitted to issue stablecoins, 4) stablecoin issuers are now subject to anti-money-laundering rules and the Bank Secrecy Act, 5) stablecoin issuers must be able to freeze, burn, and seize tokens, 6) stablecoins must be immediately redeemable for a US dollar, and 7) issuers can not pay interest on stablecoin deposits. What the act imposes is that stablecoins simply act as plumbing: they are not an asset like a tokenized money market fund, they are not a bank deposit that can be reinvested by issuers elsewhere, and they are safe, secure, and immediately redeemable 1:1 at all times. In short, the GENIUS Act derisked stablecoins for any American participants. Stablecoins no longer operate in a legal gray area, and their breadth is expanding now more than ever.

Stablecoins Now and in the Future

In the wake of the GENIUS Act, stablecoins have begun to truly blossom as not just a liquidity instrument for crypto markets, but as a legitimate means of payment, cross-border transfers, and US dollar exposure. We will break down the markets which stablecoins have currently penetrated and which they are anticipated to capture a share of, discuss the competitive dynamics at play and the justification for stablecoin demand, and provide a subsequent assessment on how much of a given market can realistically be addressed in a 10-year time frame. The publicly available information on the size of the markets analyzed typically comes in the form of annual transaction volume, so to estimate the actual USDC liquidity needed we use the formula: Liquidity Needs = (Annual Transaction Volume) / (365 / Average Holding Period), where average holding period is the number of days for which USDC would be held for a given transaction type. We provide our estimates for the liquidity needs of each market in their respective sub headers below.

Cryptocurrency Markets: ~$40 billion

Cryptocurrency markets globally are worth roughly $2-3 trillion USD, although prices do fluctuate quite radically. Approximately 60% of said value stems from Bitcoin, essentially the only algorithmic cryptocurrency which we would assign any amount of validity to. In spite of this, it does not appear that the market as a whole is going anywhere soon. The crypto market requires roughly $200 billion of stablecoin to function at present. Stablecoins will always serve the crypto market’s needs in full, so estimating how large the crypto market’s needs are is purely dependent upon crypto pricing going forward. As most are aware of, this is an extremely difficult thing to predict. To us, cryptocurrency does indeed serve a purpose and will never be worth zero. Assuming that legitimate crypto demand is presently satiated and perhaps that a portion of present demand is illegitimate (speculative trading, etc.), it seems reasonable to assume that crypto markets as a whole (excluding stablecoins and other tokenized assets) could be worth about the same as they are today in 10 years time once accounting for inflation.

In cryptocurrency trading, Tether is the larger player as compared to Circle. Tether founded 4 years earlier and thusly has always had more USDT in circulation in the crypto market. Although Tether has proven to be somewhat untrustworthy in the context of the centralized system, it is entrenched in the crypto market and still serves traders who prioritize large scale, immediate liquidity over reliability and compliance. Going forward, it is reasonable to expect Tether to hold this advantage (~70% share) over Circle, meaning that in an equivalently sized market ten years from now, we see ~$40 billion in stablecoin demand for USDC coming from crypto markets.

Remittances: ~$0.8 billion

Remittances, or remittance payments, are payments sent from foreign workers back to their home countries. On an annual basis, approximately $900 billion USD flows through the traditional banking system in remittances, although the true value of remittances likely far exceeds this as it is difficult to account for the flows of cash or hawala systems. Some examples of major corridors would be the United States to Mexico, the Gulf States to India, and Europe to Northern Africa, with India receiving ~$130 billion annually and Mexico nearly $70 billion.

When using the traditional banking and remittance system, remittance payees lose 5-10% of their payments and are subject to wait times of 1-5 days. Using the stablecoin system, payees lose 0-1% of their payment value with instant payment settlement. Additionally, stablecoins are far more accessible as individuals do not need a bank account to access decentralized platforms (~1.4 billion people without a bank account globally), and payments can be made via smartphone 24 hours of the day. Stablecoins are, in this case, an unequivocally better system than the traditional digital payments platforms and could also feasibly capture a large fraction of the cash and hawala market on convenience alone.

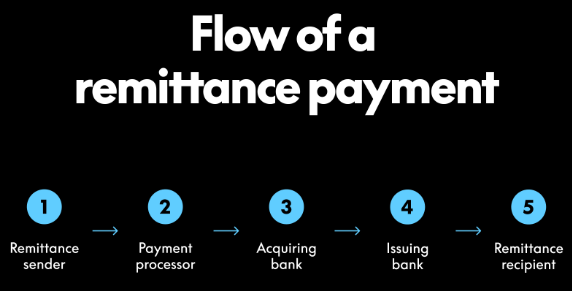

Traditional remittances flow through either specialized remittance companies like MoneyGram and Western Union, or through traditional banks like JPMorgan Chase when payments are larger in size. One of the problems for traditional institutions is that their payments infrastructure was built decades ago and is not readily modified. Banking systems are inherently immobile due to the regulatory pressure placed upon them, and evolving legacy systems for real-time settlement would be impossible without major capital investment. Another issue is the geographic fragmentation of banks. When a remittance payment is sent, a payment processor, a local bank, and a foreign bank must all earn margin. This, along with the physical infrastructure and compliance teams which banks must have, means that traditional remittance systems will never be price competitive with a blockchain system.

Figure 4: Traditional Remittance Payment Structure

Source: PayPal

In spite of this, stablecoins will not likely be able to capture all of remittance payments demand. Beating banks on trustworthiness is not a reasonable proposition, and although banks can not beat the blockchain on cost, they can and will cut costs to a certain degree. Alternatively, certain legacy remittance players like MoneyGram have actually integrated USDC into their system in order to offer customers a service with a traditional finance trustworthiness and improved costs and convenience by way of the blockchain.

Going forward we do not see a reason for global remittances to grow as a percentage of global GDP, so at ~$1 trillion in annual value per year at present, we can see the market being just over $1.2 trillion 10 years down the line. Analysts estimate that stablecoins could feasibly capture 30-50% of remittance flows annually: at 40% of transaction value and assuming that stablecoins are held for only two days before being redeemed (an extremely conservative estimate as many international citizens will hold USD in wallets for its stability), remittances would require ~$2.6 billion in stablecoin demand. Of this $2.6 billion in demand, we conservatively estimate that Circle can capture ~30% of such (constant relative to current levels). This sums to roughly $0.8 billion in USDC demand.

Ultimately the value in remittances for stablecoins is not so much in the financial gain from remittance payments, but rather that it serves a wedge for further adoption. Customers making remittances by way of decentralized exchange become much more likely to use the decentralized system for other beneficial processes which we will discuss below, further increasing stablecoin demand.

Digital Payments: ~$105 billion

On an annual basis, approximately $1.8 quadrillion in digital payments are made, generating ~$2.4 trillion in revenues for banks and associated payments companies. Of this $1.8 quadrillion only a fraction is addressable in the context of stablecoins, however given the size of the pie a tremendous opportunity exists.

Of the $1.8 quadrillion in payments made annually, roughly $60 trillion are consumer purchases, $120 trillion are business-to-business transactions, ~$700 trillion are capital markets related, and ~$900 trillion are interbank transfers. In general payments infrastructure is quite efficient and cheap, but niches where stablecoins can create newfound value do exist in scenarios where systems are currently slow, fragmented, and expensive.

Cross-border B2B Payments: ~$37 billion

In the context of payments, cross-border B2B payments are a significant opportunity for stablecoins. The inefficiencies seen in remittances are essentially identical in the case of import and export payments, supplier payments, and other B2B needs. Bank transfer settlement takes days rather than seconds, costs are in the magnitude of 50-200 bps, and because of the systems in place, banks will not be cost competitive now or in the future. Similarly to remittances, certain institutions have adopted Circle and Tether’s offerings for internal use, while other institutions like JPMorgan have created their own blockchain payments infrastructure with the JPM Coin as a competitive response. Although JPM Coin does not have the same liquidity as something like USDT or USDC and can only be used for internal JPMorgan purposes, it can help to lower costs for banking players and help hold on to market share in the face of an objectively better system. Altogether, cross-border B2B represents nearly $100 trillion in annual flows of which we could see stablecoins capturing a significant share. A realistic long term expectation is that stablecoins capture 30-50% of traded value, with the remaining portion remaining on a pressured legacy system that lowers costs and succeeds as the trustworthy incumbent. Of this ~$40 trillion, we anticipate that USDC will capture a larger share than Tether due to their reputation as being compliant, trustworthy, and stable. Given their 30% share of crypto markets, we could see Circle conservatively capturing 50% of B2B markets for the reasons above. Assuming that B2B funds are required for an average of 1.5 days, we see a ~$37 billion market for USDC in cross-border B2B payments.

Merchant Payments: ~$0 billion

Roughly $45 trillion in transactions occur annually on credit card networks, generating ~$1 trillion in revenues at fee rates of 2-3%. Credit card purchases typically flow through four intermediaries: the point-of-sale system (charges fees to merchant, somewhat indirect fee on consumers), the acquiring bank (physical bank who acts on behalf of merchant), the card network (Visa, MasterCard, American Express; routes payment requests between acquiring and issuing bank), and the issuing bank (acts on behalf of consumer). Each of the four intermediaries institutes their own checks and balances and has their own operating costs to account for. With stablecoins, the consumer transfers to the merchant directly and settlement is handled instantly with fees in the range of 0.1%. Once again, stablecoins are the most efficient system.

Because of the exploitable inefficiencies at hand, both Visa and MasterCard have begun to implement stablecoin technology for back-end settlement, with Visa recently instituting a pilot program using USDC for bank-to-bank settlement purposes. Visa has also pledged to operate a node on Circle’s new stack of blockchain infrastructure, Arc, along with involvement from other major financial players including Goldman Sachs, Commerce Bank, Deutsche Bank, Standard Charter, BNY, State Street and HSBC. Visa’s program seeks to integrate blockchain systems to streamline settlement between acquiring and issuing banks, cutting back on the multi-day settlement timeline which has previously been in place. For the acquiring and issuing banks, the system is also preferential as faster access to funds means greater optionality for financing and a presumably lower cost of capital. In short, settlement via stablecoins is an intuitive solution for this use case and has strong incentives for adoption in all players at hand. For Visa settlement is faster and cheaper, for banks liquidity is improved, and for merchants fees will likely come down slightly.

This pilot is not the same as Visa instituting stablecoins for payments at the merchant’s till; because of the frictions surrounding consumer behaviour we actually see this as one of the lowest likelihood and longest timeline opportunities for stablecoins. For the purposes of our report, we will assume that there is zero consumer adoption of stablecoins in a 10 year time frame. Regardless, back end settlement from merchant payments is a significant opportunity for stablecoin demand, one which we will delve into below.

Bank-to-Bank Settlement and Liquidity Transfers: ~$68 billion

As previously stated, interbank transfers account for ~$900 trillion of the ~$1.8 quadrillion in payments made on an annual basis. About 33% of interbank transfers are used for liquidity purposes, representing roughly ~$300 trillion in annual transaction value. Given the billions of dollars which banks tie up in the process of bank-to-bank liquidity management transfers and the poor foreign exchange rates which international banks can receive in legacy systems, there are very strong incentives for banks to switch back end payments and transfers to the blockchain. It is possible that banks move towards issuing their own stablecoins (like JPMorgan with JPM Coin), however it is hard to picture this being economically feasible for every single bank to do. Ultimately making transfers on existing blockchain infrastructure is very cheap, building a brand new system is not, and operating a bank-native system would cost the same or more than running it with Circle; the bank’s only losses are a couple of hours of interest on the dollars being transferred. Although it may be feasible for the largest players to issue their own coins internally, we don’t see it as a reasonable base case, and there exists a very large opportunity in bank-to-bank payments involving smaller players regardless. We believe that almost the entirety of liquidity transfers and bank-to-bank settlements could convert to being done in stablecoins in the long term, and given the fragmentation which bank issued stablecoins would create, we conservatively see third-party stablecoin issuers capturing 50% of volumes. More than any other use case, banks will redeem stablecoins very quickly, potentially every 4-5 hours or so. Using our required liquidity formula and assuming funds are redeemed every 4.5 hours, we estimate a ~$90 billion market for interbank stablecoin demand. Of this ~$90 billion market, we believe that Circle will capture the vast majority given their growing incorporation with the traditional banking system, and simply on the basis of Tether’s poor track record in New York. Conservatively, CRCL could capture 75% of market share for a total mature market demand of ~$68 billion.

Corporate Treasury: ~$41 billion

International corporations constantly transfer funds between accounts and across international borders. The frictions and costs of banking internationally create an easily addressable niche for stablecoin issuers in a similar fashion to remittances and cross-border B2B payments. Corporate treasury transfers represent approximately $25 trillion in annual value, all within a fragmented, high cost environment. By unifying the transfer environment on the blockchain and offering essentially zero costs, analysts believe that stablecoins could feasibly capture 50-70% of transaction value, a larger portion than in B2B payments as the entrenchment and trust factor of banks plays a smaller role on an internal scale. Similarly to in the case of cross-border B2B payments, we believe that Circle can benefit from their regulatory reputation and capture an outsized portion of this market (~50%). Assuming a holding period of two days and a stablecoin market capture of 60%, corporate treasury needs could easily translate to ~$41 billion in USDC demand.

International USD Savings and Cash Holdings: ~$165 billion

The US dollar is, in a way, the world’s currency. It is impossible to find a currency that is more stable, reliable, and universally recognized. Especially in the context of markets like Argentina and Venezuela, it is easy to picture a demand for US dollars simply as a store of value or a hedge against local inflation. Individuals receiving remittances by way of stablecoins are even more likely to hold onto USD stablecoins in savings in order to avoid paying foreign exchange spreads repetitively and to avoid local currency risk. For these reasons, there exists a significant demand for US dollars simply for the purpose of holding savings, both on an individual and corporate level.

With the emergence of tokenized assets (more on that later), we see the majority of foreign savings in decentralized markets flowing to these interest bearing funds rather than sitting as USDC. Given the background of roughly $30 trillion in household savings in developing economies, we could feasibly see 0.5% of this market sitting as USD stablecoin savings year round. Assuming that CRCL captures 30% of that volume (constant compared to current market share in similar markets at present), this is a ~$45 billion market for USDC.

Additionally, there is about $1.5 trillion in physical USD cash outside of the United States. This cash exists as holdings for foreign banks, businesses in both dollarized and semi-dollarized economies, and for the purposes of the shadow economy. With time, we could see a large portion of this demand moving towards stablecoins, especially in the context of foreign banks and businesses who could see benefit from not delivering physical cash and instead sending it with the press of a button. In the context of the shadow economy, it will be difficult to comply with stablecoin anti-money-laundering regulation and the like, so we do not see a large portion of this demand being captured. Overall, we can see stablecoins capturing at least 20% of the demand for physical cash outside of the United States in the long term, representing demand for ~$300 billion in stablecoin demand. Of this demand, we see Tether holding a slight advantage to Circle due to Tether’s prevalence in foreign markets, and can realistically see Circle capturing 40% of demand representing ~$120 billion in USDC.

Tokenized Assets: ~$200 billion

Tokenized assets are perhaps the largest and most intriguing potential source of demand for stablecoins. Tokenized assets take a similar form to stablecoins in that they are sold on decentralized exchanges and are backed 1:1 by assets like US Treasuries, money market funds, commodities, private credit funds, equities, and real estate assets. It is safe to say that there is a very large global demand for assets of this kind (especially assets from American capital markets), and as a result both Franklin Templeton and Blackrock have initiated selling tokenized securities. As it stands, there are billions of dollars in tokenized treasuries outstanding alone and the expectation is for demand to continue to skyrocket.

Foreign demand for tokenized assets can stem from governments and their central banks, private banks, corporations, institutional investors, and everyday individuals alike. All of these entities have savings and investment needs, and almost all of their needs are best met in American capital markets. In spite of this, it is currently a tedious process to actually secure holdings in desired assets for a large portion of this demand. Take US treasuries as an example. Any international entity demanding US treasuries needs a US brokerage account, but for the sake of compliance risk brokers like Charles Schwab, Fidelity, and International Brokers restrict the countries in which they will allow individuals to run an account from. Even if a brokerage account can be secured on the American end, many developing nations have tight controls on the flow of funds for international investment purposes. If our international actor is actually able to secure a brokerage account, they must then transfer their local dollars into said brokerage account via traditional banking system, which we have already established to be slower and more expensive than blockchain transactions. Then, once funds are in an American brokerage account, there are high minimum investments on a number of government debt products and investment minimums in the order of magnitude of hundreds of thousands of dollars on many private funds. When buying a tokenized asset, our actor simply transfers funds into a decentralized wallet and buys the tokenized asset with instant settlement. There are no issues with securing a brokerage account, local authorities can not prevent the flow of funds, foreign exchange and transfer fees are essentially zero, and investors can purchase fractional portions of any asset they desire. It is an unequivocally better system for many who can currently access American capital markets, and an exciting prospect for those who currently can not.

Analyst’s expectations for tokenized asset demand in the long term are highly variable: it is difficult to predict given the fact that tokenized assets may not simply capture existing global asset demand but will also augment it or be additive. In the context of ~$500 trillion in foreign asset holdings, even a small additive effect or capture of present share is significant. Most professional opinions are in the context of a 4-5 year timeframe and estimate stablecoin demand at ~$5-$30 trillion (Boston Consulting Group, Citigroup, Standard Chartered estimates). On a ten year time frame, we believe that ~$20 trillion in tokenized asset demand is both realistic and conservative, representing ~3% of global asset demand. If the average global asset transaction requires stablecoins for a period of five days, this requires about $275 billion in stablecoin demand. Due to their regulatory standing in the United States, we see Circle capturing the majority of tokenized asset demand for ~$200 billion in long term demand.

Aggregate Demand: >$550 billion

In aggregate, we can conservatively estimate that in a 10 year time frame demand for Circle stablecoins, namely USDC, will exceed $550 billion, an over 600% increase from current levels of ~$75 billion.

In a way, estimating all stablecoin demand drivers separately is a suboptimal approach as demand between use cases is deeply intertwined. A given demand driver will likely pull an actor in, and it is then much more convenient for them to use the decentralized system in other cases as well. In the context of an international investment fund, tokenized assets may be what pulls them into the decentralized system, but they will also require stablecoins for treasury and international payments purposes. In the context of an international corporation, stablecoins may initially be used for internal international transfers, and then implemented for investment purposes in tokenized assets and in B2B payments. Ultimately the value proposition is much larger in aggregate than it is on a standalone basis; this is not a standalone service but rather a novel financial system. If anything, this could signal that we have greatly underestimated the total demand for stablecoins in the long term.

It may be easy to remain skeptical, but we believe that the incentives are in place for stablecoin demand to skyrocket, and incentives drive decisions in the long term. Stablecoin transfers are faster, cheaper, and accessible to a broader base of actors than the alternatives. Payments firms like Visa and MasterCard and institutions like Franklin Templeton and Blackrock are not players that we see pursuing pennies; they are the firms on the cutting edge of trillion dollar opportunities, and that is how we view the internet financial system on a go forward basis. Circle has already proven that it can grow stablecoin demand over 70% year-over-year in weak cryptocurrency markets, and we can see similar growth being achieved in the long term in order to satiate what will likely be billions of dollars of stablecoin demand from growth in decentralized finance.

Corporate Governance and Management Alignment with Shareholders

Circle is led by co-founder, CEO and Chairman Jeremey Allaire. Prior to founding Circle, Allaire played major roles at a variety of other software and technology firms including Chief Executive Officer of Brightcove, Chief Technology Officer of Macromedia, and co-founder and Chief Technology Officer of Allaire Corporation.

In general, the Circle management team exudes impressive levels of competence in what we see as the key skillsets for CRCL: software development, financial markets and financial infrastructure management, and legal expertise. Notable mentions include President and Chief Legal Officer Heath Harbert, the previous Chief Legal Officer of Citadel Securities and the 14th chair of the CFTC, Chief Financial Officer Jeremy Fox-Green, previous Chief Financial Officer of McKinsey & Company North America, and Li Fan, previous Chief Technology Officer at Lime.

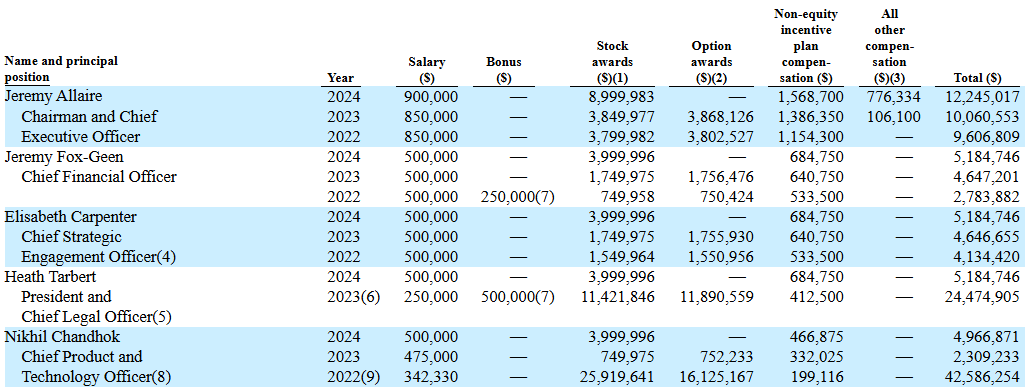

Circle’s executives are compensated using a combination of fixed cash salary, a short term incentives plan (STIP), and a long term equity incentives plan. Fixed salary tends to represent approximately 7-10% of total compensation, a low number which we can appreciate as investors. Circle’s STIP pays out incentives based on the achievement of adjusted EBITDA goals, which we like as a proxy for free cash flow, and on the accomplishment of a variety of platform expansion goals. Last fiscal year, some of these initiatives included the closing of three enterprise-scale commercial partnerships, the opening of accounts with three new reserve banks, and the launching of three components of major blockchain infrastructure. Long term equity awards operate in a similar fashion, with a focus on RSU’s that are both time based and performance based. Figure 5 shows Circle’s summary compensation table.

Figure 5: Circle Summary Compensation Table

Source: Company Filings

Shared-based awards typically account for >75% of total executive compensation, something which we see as a tremendous positive when combined with CRCL’s clawback policy as well as no hedging or pledging requirements.

In conjunction with their equity compensation strategy, Circle exhibits strong insider ownership in both the management team and board, another positive signal from an investment perspective.

The Circle board consists of eight members, of which all members are independent except for Jeremy Allaire. Similarly to the management team, CRCL’s board boasts exceptional qualifications in relevant areas, with highlights including Craig Broderick, former Chief Risk Officer of Goldman Sachs and current member of the board of Bank of Montreal, Adam Selipsky, former Chief Executive Officer of Amazon Web Services as well as former Chief Executive Officer of Tableau Software, and Rajeev Date, Managing Director of venture capital firm Fenway Summer.

In summary, Circle’s corporate governance scene boils down to two key points: the right people are in place to realize success in the long term, and the right incentives are in place to push them towards success. The company ticks all of our boxes and our confidence in the stablecoin story grows.

Valuation

CRCL currently trades at just over 40x enterprise value to forward EBITDA, a reasonable value for a high growth, highly scalable tech platform and in the same order of magnitude as names like CrowdStrike (~60x), Palo Alto Networks (~33x), Snowflake (~67x), and Shopify (~61x). CRCL has only been publicly listed for less than a year, but relative to itself it is currently trading quite low. Figure 6 shows CRCL’s relative valuation.

Figure 6: Relative Valuation

Source: S&P Capital IQ, Phi Research

Given the radical and persistent growth which both us and other analysts expect for CRCL, we think that the most appropriate means of estimating an intrinsic value for shares comes in the form of discounted cash flows modelling. We will start with Bloomberg analyst’s consensus numbers for revenue and EBITDA over the next four years and then model an additional six years of growth using our long term expectations for total USDC supply. We believe that sell-side analyst expectations are often relatively accurate on controversial American names like CRCL (24 covering analysts, price targets ranging from ~$80-$300) as a balance of overly bullish and overly bearish positions can be found.

Recall that USDC generates Circle revenue not through transaction fees, but through interest earned on short term, highly liquid securities. Although CRCL does issue stablecoins that are not US dollar denominated, we see this as a very limited market and will not include such drivers in our model. We model total demand for USDC to reach ~$550 billion in a ten year time frame, and have estimated treasury rates to slowly decrease to ~3% over time. 3% rates are closely aligned with inflation goals of American policy makers and are a reasonable and conservative expectation for a long term average. Although 10 year government securities yield over 4% while 1 year rates are ~3.6%, and it would be possible to solve for the implied 1 year interest rate for each period over the next ten years geometrically, we believe that this approach would overestimate the interest CRCL will earn. This is due to the natural upward slope of the yield curve which is a result of treasury liquidity and the additional risk taken on longer term securities, not due to the fact that rates are expected to rise over time. For these reasons and for the sake of conservatism in modelling, we have opted for the approach of modestly decreasing rates over time.

Bloomberg analysts project CRCL to realize significant EBITDA margin expansion in the medium term, a reasonable assumption as CRCL is essentially a software platform. Costs associated with maintenance and scaling of the network are very limited, and as a result we have modelled margins to reach 36% in the long term. This is similar to lower margin SaaS and technology platform businesses, and in reality we could see Circle achieving levels in line with higher margin SaaS companies (~50%) or even pushing for levels similar to payments companies like Visa and MasterCard (~70%). To maintain a margin of safety on our valuation, we use 36% and assume a somewhat bearish scenario for margins going forward. In respect to free cash flow conversion rates we have done the same, assuming that CRCL converts at a rate in line with some of the weaker performing SaaS peers (~70%), in spite of the fact that the company has converted at over 80% historically.

Figure 7 shows our complete discounted cash flows model. Our base case brings us to a share price of $216.18, a significant step above today’s close of $118.09.

Figure 7: Discounted Cash Flows Model

Source: Bloomberg, Phi Research

The remaining two assumptions we must make are surrounding CRCL’s cost of capital and an appropriate exit multiple to use. Estimating cost of capital using traditional CAPM and WACC methods is not viable for Circle as the company has only traded publicly for less than a year, so we will start by applying some intuition on what long term beta values the company could exhibit. Circle is in many ways a countercyclical business, as higher interest rates mean significantly higher revenues for the company. On the contrary, the broad market suffers in periods of high interest rates, meaning Circle should demand a cost of capital below the market average of 8%. Additionally, demand for Circle’s stablecoins is not highly cyclical; volumes needed for tokenized assets, international savings, and bank settlement are not affected significantly by broadscale economic downturns. Because of the resilience of payment’s and financial exchange’s business models we see companies like Visa and Mastercard with beta’s in the range of 0.7-0.8, and institutions like TMX Group and CME with beta’s just slightly above 0 (in conjunction with strong returns, not a poorly performing industry). Taking this into account it would be feasible to argue CRCL for a cost of capital in the range of 5-6%, however given the uncertainty of growth levels going forward we see somewhere in the range of 8% as a more conservative estimate.

In regards to an exit multiple, we believe that 10x is a good bottom end for CRCL as this is a level shares could realistically trade at in the case that growth is essentially zero beyond 2036. In the case that 5 or so years of ~10% growth lay ahead at the time, we could see the company trading at or above 30x. The truth usually lies somewhere in between, and we have chosen 17.5x as an exit multiple, representative of a mid single digit growth, high margin platform business.

Our model is highly reliant on a number of assumptions which we can not rigorously back. Although we have

taken no liberties thus far in estimating the growth which CRCL will accomplish, and these expectations for growth have proven sufficient to justify investment, it is important to analyze a variety of scenarios which could realistically occur. To start, we have prepared the below table analyzing the impact of our cost of capital and exit multiple assumptions on current intrinsic share value.

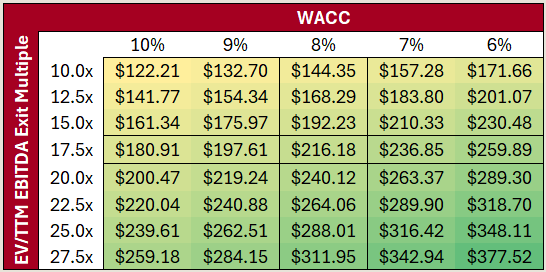

Figure 8: Sensitivity Analysis – WACC and EV/TTM EBITDA Exit Multiple

Source: Phi Research

Regardless of the scenario analyzed, it would appear that CRCL is undervalued at present (closing price of $118.09 today).

What is perhaps the most important moving piece in our model and the one for which we see the largest distribution of potential outcomes is our 10 year estimate for USDC demand. In international savings for example we have assumed that stablecoins are able to capture 0.5% of demand in the long term. If in reality stablecoins capture 1% of the market, this would represent an additional ~$200 billion in USDC demand over our assumed estimate of ~$550 billion. In respect to tokenized assets, we assumed that 10 year transaction value levels would be roughly $20 trillion annually, however certain credible analysts have estimated levels to be 50% higher in half the time. This would imply that we may have excluded additional hundreds of billions of dollars is USDC demand from our model. The same principles apply in the downward direction as well, however there is a limit on how wrong we may have been (100%) whereas on the upside there is not. In addition, we believe that we have provided somewhat modest estimates for the size of long term USDC demand, and that there are probabilistically many more scenarios above our base case than below it.

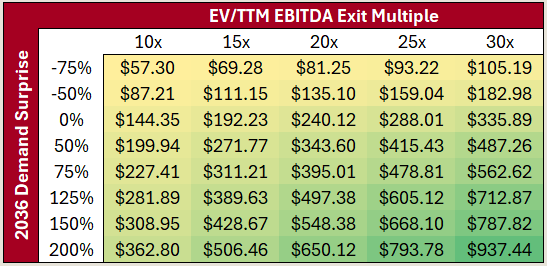

Figure 9: Sensitivity Analysis – EV/TTM EBITDA Exit Multiple and 2036 Demand Surprise

Source: Phi Research

Assuming that CRCL can only capture one half of our forecasted long term demand, current share prices are still justifiable. In the case that we have radically overestimated long term demand by 300% (-75% demand surprise), the downside for CRCL shares is still only within the range of 50%. Scenarios where demand beats our forecast by 100% or even 200% are plausible given the size of the pool of capital which Circle could potentially address (quadrillions of dollars), and in any of our upside scenarios the company will deliver gains in the range of many hundreds of percentage points.

Conclusion

The story of Circle Internet Group is one which comes with a great degree of uncertainty, namely surrounding the question “how big will stablecoins get?” Circle’s products exploit major inefficiencies in current systems with significant support from American regulators, all while there is a lack of mobility or feasible investment response from legacy competitors. Taking this into account along with the involvement of massive players like Visa, Blackrock, and a list of international banks as a form of risk abatement, we can confidently say that the answer is “big enough”. Even in the case that stablecoins greatly disappoint consensus expectations for the markets they can feasibly address, Circle shares are roughly adequately valued. In the case that the company surprises on the upside and captures a single additional percentage point of potential demand, we likely have in front of us a long term multi-bagger. The upside far outweighs the downside, and on a balance of probabilities, CRCL shares far outperform the broad market. Strong Buy.