Kits Eyecare Ltd. (TSX: KITS), Removing the Rose Tint

Published on 2026-02-26

Kits Eyecare Ltd. is a Canadian direct-to-consumer online provider of prescription glasses, sunglasses, and contact lenses. The company currently trades at a premium valuation due to its continuing strong revenue growth and anticipated future increases in margins. Based on the competitive landscape of the business and financial estimates, we believe the company is significantly overvalued and that investors should short sell.

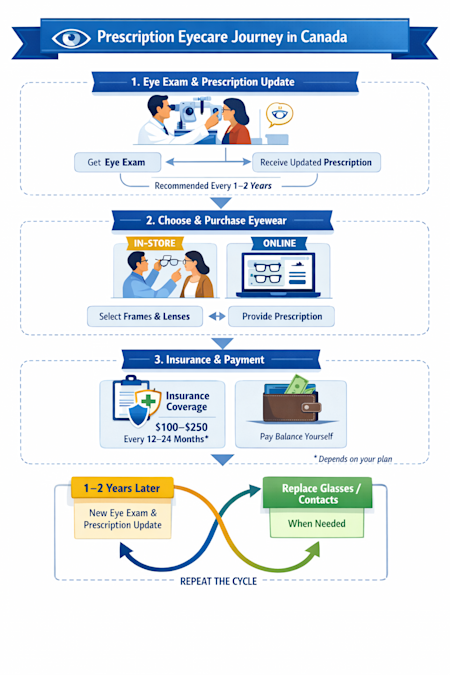

Kits Eyecare Ltd. is touted as a disruption to the traditional Canadian prescription eyecare market, and in a certain respect it is. In general, individuals in Canada will visit the eye doctor every 1-2 years, depending on the condition of their eyes, their insurance coverage, and their personal preferences around their optical health practices. Upon examination, individuals will be granted a prescription for optical assistance (i.e. the specifications of a contact or glasses lens which will best assist their vision) with a duration of 1-2 years. Traditionally, patients would immediately purchase a new set of glasses or a contact lens subscription from their eye doctor, however online retailers like Kits have recently surfaced, offering patients the option to send them their prescription and select from hundreds of frame options in the context of glasses, as well as the option to purchase a contact lens subscription. As it stands, online eyewear purchases account for roughly 13% of annual transaction value in Canada (contacts are ~23% online), a share that is expected to continue growing in the near term.

Figure 1: Canadian Prescription Eyecare Cycle

Source: Phi Research

In many ways it is much less convenient to purchase your eyecare products from Kits as compared to an eye doctor; there are essentially two added steps in needing to transfer both your prescription and insurance information to Kits as compared to immediately making a purchase on sight. Additionally, most individuals have a preference for trying on eyewear in person (assuming constant costs). Given the sensitivity of the facial area and the consistency with which consumers wear their glasses, it is critical that consumers find a frame that they find comfortable, stylish, and fits well, and in spite of online try-on tools and the integration of AI in the area, it is not possible to create an online experience that matches brick-and-mortar try-ons.

As is such, Kits competes as a lower cost alternative to purchasing with an eye doctor, with their vertically integrated design and lens finishing process enabling them to do so (although they are not vertically integrated whatsoever in the contacts space). Kits low-cost model has allowed the company to roughly double revenues over the past four years, with the company beginning to generate positive EBITDA and free cash flow at YE 2023.

Competitive Analysis

In spite of Kits ability to generate strong top line growth since their 2021 IPO, the company has struggled to realize success on the bottom line, with EBITDA margins sitting in the ~5% range as of late. Although gross margins are not impressive (~33-35%), the driving force behind Kits lagging EBITDA performance is their marketing spending; a requirement to acquire (and in a certain respect, to maintain) customers in a market with limited barriers to entry and intense competition.

Brick-and Mortar Competition

As stated above, Kits is a ‘disruptor’ of traditional brick-and-mortar eye doctor sales. Brick-and-mortar eyecare sales come from four types of competitors: independent eyecare clinics, independent eyewear stores, vertically integrated clinics, and big box retailers like Walmart or Costco.

Independent Eyecare Clinics

Independent eyecare clinics purchase their contacts and glasses from third party manufacturers, often placing an emphasis on higher quality brands in the glasses space to maintain margin and to play into their primary role; they are not the cheapest option, simply a very convenient choice and by far the most trusted: your friendly neighbourhood eye doctor. Although pricing is not their strong suit, independent clinics still often provide glasses brands at a lower price than consumers could purchase them for by themselves (think brands like Ray-Ban, etc.). Unlike in other consumer goods like clothing, consumer trust is vital in eyecare as the product is crucial to the health and wellbeing of the consumer. This and the proximity of doctors to customers is what allows the independent clinic model to exist. Although they may not have the strongest competitive standing in the Canadian eyecare space, they will always maintain a significant portion of market share for the above reasons, in spite of their inability to compete on price with other peers.

Independent Eyewear Stores

In spite of the convenience of purchasing eyewear simultaneously with the acquisition of an optical prescription, eyewear stores which are independent of any eye doctor service exist. These stores exist to service a luxury, or an especially fashion forward group of individuals; think of an Oakley or Ray-Ban store or brick-and-mortar locations of fashion focused brands like BonLook or Bailey Nelson. Notably, both Ray-Ban and Oakley are owned by EssilorLuxoticca, a highly vertically integrated parent company of many eyecare subsidiaries and a company who can outcompete Kits on cost. Additionally, nearly all independent eyewear stores are associated with an online retail store, meaning that even if customers find it inconvenient to get their fashionable glasses in-person, it is no less convenient to purchase them online than it would be to go to Kits. These stores and their associated e-commerce platforms may be less convenient than purchasing from an eye doctor, but they are able to compete due to offering specialized, well-respected products, something which Kits can not match.

Vertically Integrated Clinics

Clinic chains such as LensCrafters and PearleVision offer brick-and-mortar sales and in house clinics at the same location. With both of the above brands being owned by EssilorLuxoticca, their lens and frame manufacturing, lens finishing, design process, and logistics and retail environment are all vertically integrated, meaning these brands see the benefit of buying power in input markets and lose no margin anywhere in the value chain of their products, top to bottom. Although Kits is somewhat vertically integrated, the manufacturing process of their lenses and frames is outsourced, and even in the case that it wasn’t they would not exhibit nearly the same buying power in input markets due to their size. As a result of their degree of vertical integration and the convenient nature of buying at the clinic, vertically integrated clinics offer one of the strongest value propositions out there. In relation to Kits, vertically integrated clinics are significantly more convenient, and brands owned by EssilorLuxoticca can exhibit pricing power due to their higher relative degree of vertical integration. The only space in which vertically integrated clinics do not directly outcompete Kits is in ultra low cost eyewear, a tricky and low margin space.

Big Box Retailers

Retailers like Walmart and Costco have recently expanded into the eyecare space, contracting eye doctors to offer their services in house, and using their scale as buying power over third party glasses and contacts manufacturers. Eyecare cash flow generation works similarly to other products sold at these retailers; the margin is low but the scale is massive. Having eye doctors in house enables the entire process and makes it very convenient for customers to get their prescription, glasses, contacts, groceries, clothing, Christmas gifts, and a laundry list of other consumer goods all in one place. This convenience effect is especially strong in the case of contact lenses as contacts must be replaced on a monthly – quarterly basis. Now, instead of picking up contacts requiring its own trip or being done through a third party online service, you can pick them up on any given Sunday grocery trip. Big box retailer’s services are the ultimate in convenience for a large portion of consumers, and as a result they will hold a significant portion of eyecare market share going forward.

E-Commerce Competition

Most of the aforementioned brick-and-mortar competitors do offer online sales, but in this section we will focus on competitors whose specialty is e-commerce. There are a number of e-commerce pure play companies operating in Canada such as Zenni Optical and Eyebuydirect who are capable of beating Kits on glasses pricing, although in general these are smaller competitors. The two largest competitors which Kits faces in e-commerce are Clearly and Warby Parker, the latter being an American vertically integrated player with Canadian operations and the former being a Canadian e-commerce subsidiary of EssilorLuxoticca, the worlds largest and most vertically integrated eyewear company. Although seemingly all e-commerce platforms can match or beat Kits’ value proposition, Clearly is by far the strongest competitor we see. As previously mentioned, EssilorLuxoticca controls the entire value chain in their eyewear products and exhibits very strong buying power in input markets due to their size. Although Essilor’s vertically integrated clinics do not compete with Kits on ultra low-cost products, Clearly does, and there is an apparent and visible gap in pricing of glasses products between the two platforms. Clearly also offers Ray-Ban, Oakley, and Chanel products on their site, and is advantaged in offering them compared to Kits since EssilorLuxoticca owns and manufactures for these brands.

On the contacts side, both Kits, Clearly, and other online retailers buy contacts from third parties like Johnson & Johnson. Although this leaves little room for differentiation, Kits still falls behind here as a brand like Clearly has a titanic sized parent company to exhibit buying power and secure better prices for their customers (Walmart and Costco also outcompete here as far as physical stores goes).

Analysis

Overall, we can conclude that there exist a very large number of competitors for Kits who are either lower cost, more convenient, higher quality, of higher brand notoriety, or some combination of the four. Nothing indicates that Kits will become a market leader in any of these contexts, and although this does not render the company worthless, it establishes a low ceiling for what the company can achieve on a relative basis: Kits will not be taking over the industry or be leading it in any way.

Ultimately, the best test for the competitive standing of a business is asking how easily the business could be replaced. There is very little stopping you or I from copying the Kits business model exactly, and this is indicative of a very weak competitive standing and a very harsh competitive environment that will likely intensify. Kits is less convenient, less fashionable, has less brand recognition, or is more expensive than all competitors.

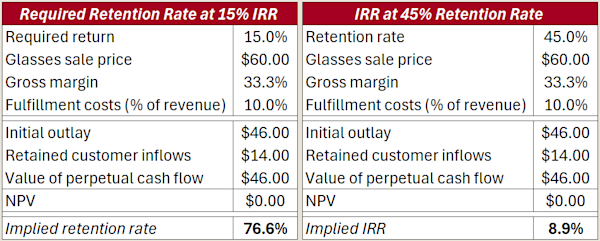

What Kits positions itself as is lower cost than name brands and higher notoriety than the lowest cost peers (this is a small niche nonetheless, despite share valuations implying otherwise). What this strategy (and the vicious competition the company faces all around) requires is a relentless and aggressive marketing campaign. Kits uses SEO tactics, influencer marketing, and even “first pair free” promotions for glasses on a rolling basis. The company even has a ‘Chief Marketing Officer’ in Angela MacInnis. MacInnis and the rest of the management team do not appear to be strong capital allocators given the fact that for a 15% IRR on a “first pair free” glasses promotion, it is required that nearly 80% customers make return purchases in perpetuity. Realistic estimates of Kits’ retention rate are in the range of ~45%, which implies an IRR below 9% on such promotions, likely below the company’s cost of capital and thus a value destroying initiative. Figure 2 shows our analysis, using gross margins and fulfillment costs in line with historical levels and estimates, an arbitrary glasses price of $60.00 (does not effect IRR as costs are a percentage of revenue), and assuming that returning customers buy glasses every 1.5 years in perpetuity (a wholly unrealistic assumption, in reality return customers usually only make an additional 3-4 purchases).

Figure 2: First Pair Free Promotion IRR

Source: Phi Research

Despite these weak returns on investor capital, Kits’ only competitive foothold is marketing, one which we do not believe is valid in the long term, and one which prevents margins from improving without compromising top line growth. Once again, we see a tangible and lower than expected ceiling on future growth. Marketing is the only driver of revenue growth, marketing campaigns are low return initiatives, and Kits’ share of revenue from repeat customers has actually fallen from 2022 to present (~65% to ~62%), meaning that acquiring new long term customers is becoming more challenging. The company is stuck between a rock and a hard place: slash marketing expenses (currently ~15% of revenue) and realize improved EBITDA margins with muted revenue growth, or continue growing revenue at weak margins. The market for a small cap stock will always prefer the latter, but the above analysis demonstrates that this is not an attractive investment proposition regardless.

So, given the competitive landscape Kits faces and their positioning within it, what are realistic expectations for revenue and margins in the long term? E-commerce currently accounts for ~13% of all eyewear sales in Canada, while ~23% of contacts are sold online. Other more mature e-commerce markets like clothing and electronics tend to exhibit e-commerce sales shares of ~30-40%, shares that are not growing significantly at this time. As compared to a market like clothing, eyewear products have a larger gap in convenience between a brick-and-mortar and online experience as try-on and fitment is more nuanced, and also thanks to the requirement for customers to transfer prescription and insurance specifications to online retailers. Additionally, there is an aspect of eyecare products being partly a healthcare good as compared to clothing which is purely a consumer good. This effect often drives consumers to purchase from the most trusted and personable source: their eye doctor. As is such, it is unrealistic to expect eyewear sales to reach an e-commerce share of ~30-40%, but it is realistic that it reaches 25% (roughly a double in e-commerce market size in a total eyecare market that is stagnant). In the American market, online eyecare sales penetration is just over 20% and is reaching maturity, making a mid 20%’s maturity level a realistic expectation for a nearly identical Canadian market. In spite of this, Kits stated in a 2025 conference presentation that their goal is to achieve annual revenue of ~$500M in 2029, nearly triple trailing-twelve-months revenue levels. This indicates that either Kits anticipates e-commerce to grow outside of a realistic range, or that the company captures a large and disproportionate share of the e-commerce market. Based on the lack of competitive moat surrounding the business, we do not believe that either of these scenarios are possible or in any way likely. In the long term, we can see annual revenue reaching ~$400M, indicative of a doubling in e-commerce market size (~26% future penetration compared to ~13% current) without significant changes in Kits share of said market.

When we look at more mature consumer goods companies, EBITDA margins seem to find themselves in the low teens range. Given Kits positioning, largely as a lower cost competitor and not a luxury brand or particularly notable on other features, we think the low end of more mature peers (e.g. Aritzia, Warby Parker) is realistic; somewhere in the 10-11% range. This is roughly indicative of the company cutting marketing expenses as a percentage of revenue in half compared to current levels, a steep but potentially attainable goal when attempting to maintain revenue levels.

These future revenue and EBITDA numbers represent significant growth in top and bottom line for the company, the problem rests in the fact that the growth is unsustainable, requires excessive levels of marketing investment, and that the market has priced in much more financial improvement than is actually attainable.

Corporate Governance and Management Alignment with Shareholders

Kits is led by CEO and Chairman Roger Hardy. Hardy previously founded and headed Coastal Contacts prior to their sale to EssilorLuxoticca in 2014. Hardy is essentially the only individual who is a member of the board or management team with notable credentials.

Board of Directors and Executive Compensation

Kits’ board of directors is made up of seven individuals, two of which are insiders (Roger Hardy and Arshil Abdulla, Chief Technology Officer). This is an excessively small board of directors, and there is a troubling lack of independence present. Kits does not employ any form of executive or director share ownership plan, and as a result four of five independent directors currently hold less than ~50,000 shares, with Andrew Reid only holding a dismal 1,262.

Kits renumerates its management team with a mixture of an annual cash salary and an annual incentives program. It is notable and somewhat alarming that the company does not employ some form of long-term incentives plan, as this prevents excessive risk taking and a detrimental focus on short-term results. It is easy to see this manifesting in Kits’ low return, aggressive marketing spending.

In general, Kits’ executive compensation plan is not terribly well defined. The company has both a stock option and a restricted shares plan, but has not issued any options to management or board members since 2022 (shares were in the range of $2.00-$3.00 as compared to ~$18.00 today). It is a glaring red flag to see that management no longer wants to grant options above prices as low as $2.00 per share. Kits often grants restricted shares to management as part of their annual incentives plan, however non-cash compensation only accounts for ~20% of total salary on an annual basis. More problematically, fixed salary tends to account for 50-60% of total executive compensation, meaning most of Kits’ executive compensation is guaranteed and provides no incentives for the alignment of management values with shareholders.

Insider and Institutional Ownership

Kits’ largest shareholders are CEO Roger Hardy and CTO Arshil Abdulla by a large margin. Outside of these two individuals, their holding companies, and executive Joseph Thompson, Sabrina Liak, ex-President of Kits is the largest shareholder. No single institution holds over 1.5% of Kits shares, and of those who do own over 1% of shares, only one has entered at an average price above $10.00 (as compared to today’s close of $17.53). Strong insider ownership is often a positive in an equity, but that is in the context of a strong institutional presence, a well formulated executive compensation plan, and a management team with a growing ownership stake. None of these boxes are ticked for Kits Eyecare Ltd., and we see strong insider ownership as an indicator of a lack of demand for shares in institutional markets in this case. In addition, the fact that management is not seeking to significantly increase their ownership stakes is a negative signal.

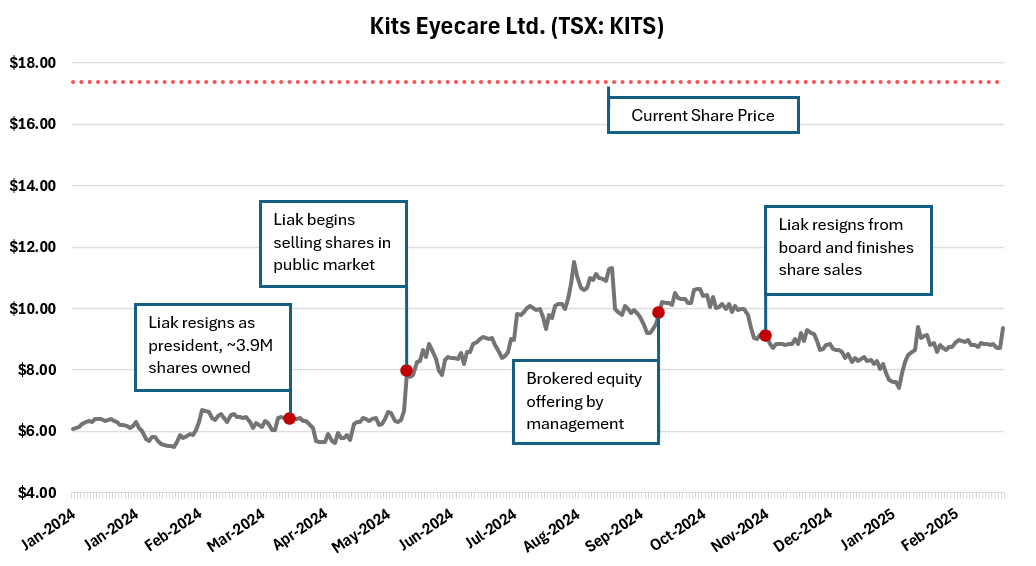

The Departure of Sabrina Liak

Sabrina Liak was previously the President and Co-Founder of Kits Eyecare. Prior to her work with Kits, Liak served as Managing Director and Portfolio Manager of Goldman Sachs growth private equity in clean energy, heading a multi-billion dollar investment fund. As compared to current board and management members, Liak undoubtedly has the most impressive credentials, however in April of 2024, it was announced that she would resign from her role as President and move to a board advisory role. At the time, Liak was one of Kits largest shareholders with ~3.9 million shares beneficially owned. In June, Liak began selling her ownership stake aggressively in the public market, and in September 2024, Liak and her spouse were a part of a brokered equity offering which saw Roger Hardy, Arshil Abdulla, and Liak sell 1.45 million Kits shares at a price of $10.15 (link). Shortly thereafter, in November of 2024, Liak resigned from the Kits board and finished selling her shares in the public market, with a current remaining position of 1.6 million shares as compared to 3.9 million previously. After leaving Kits, Liak founded Aloi Capital, an office which focuses on putting the $15-$25 million she secured from selling Kits into different investments. It is alarming to see a company’s most accredited member leave and sell the large majority of her stake for the exclusive purpose of pursuing other investment opportunities. It is also alarming to see top management like Roger Hardy and Arshil Abdulla selling shares by way of prospectus at a value nearly 50% lower than current prices.

Figure 3: Sabrina Liak’s Departure Timeline

Source: S&P Capital IQ, Company Filings, Phi Research

Overall, Kits corporate governance setting is very weak, essentially ticking none of our boxes. The management team is not exceptionally qualified, incentives are not in place that align their best interest with that of the shareholders, director quality, share ownership and independence levels are low, and top management either wants out completely or has no desire to receive risky share-based compensation anywhere near current KITS price levels. In the valuation section, we will find that it is no coincidence that management sold shares via prospectus in the $10.00 range, while no significant institutional money has flowed in above that level either. Lastly, we thought we would mention that on the 4th page of Kits’ 2024 Annual Information Form there is a ‘note to draft’ discussing how to not seem overly promotional in the document. This was accidentally left in and does not appear to have been noticed yet nearly a year later. Not a gleaming endorsement of oversight and attention to detail.

Figure 4: 2024 Annual Information Form Blemish

Source: Company Filings

Valuation

Kits currently trades at ~53x trailing twelve months EV/EBITDA and ~44x on a next twelve months basis. This is well above Nvidia (~35x and ~20x respectively), Oracle (~19x and ~13x), GE Vernova (~40x next twelve months), Rocket Companies Inc. (~21x next twelve months), and every stock in the magnificent seven apart from Tesla. What would you prefer to own? Perhaps most importantly, Kits trades well above its closest comp, Warby Parker’s, valuation levels which sit at ~32x on a trailing basis and ~22x on a forward basis.

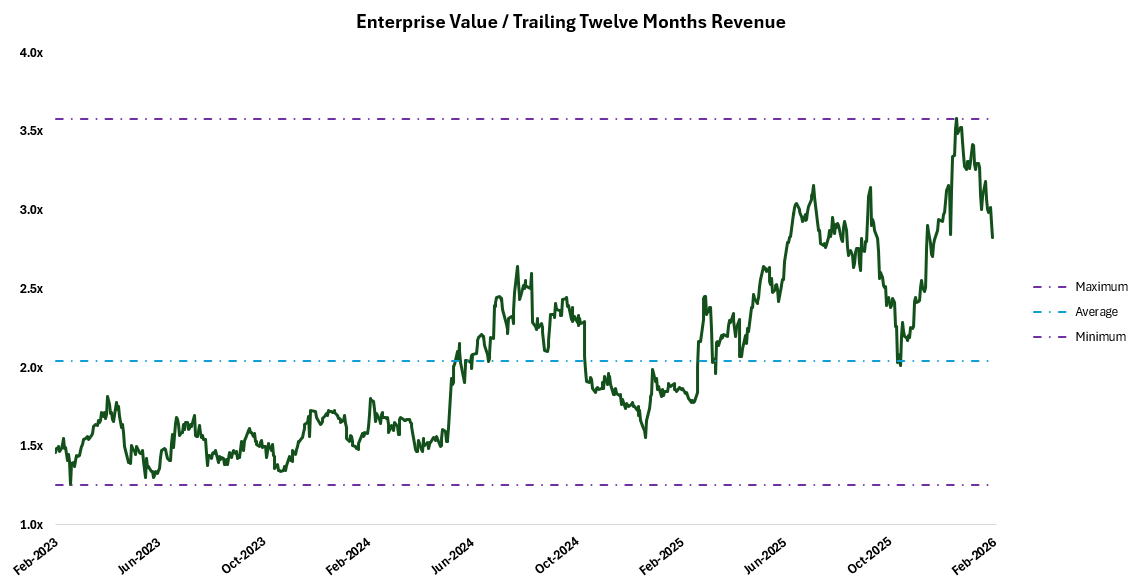

Analyzing Kits valuation relative to itself is not feasible on an EV/EBITDA basis as the company has not generated positive or significant EBITDA for the majority of its lifetime. Below we show a chart of EV/TTM Revenue, a metric which we do not grant much validity to as Kits is extremely low margin, the opposite of a software company for which this metric can be used credibly. In spite of this, bullish institutions (the same ones who broker management’s equity offerings) use the metric to attempt to justify current share pricing. Regardless, Kits trades at nearly 3x revenue, both expensive for a software company (which Kits is not) and relative to its historical levels.

Figure 5: Relative Valuation

Source: S&P Capital IQ, Phi Research

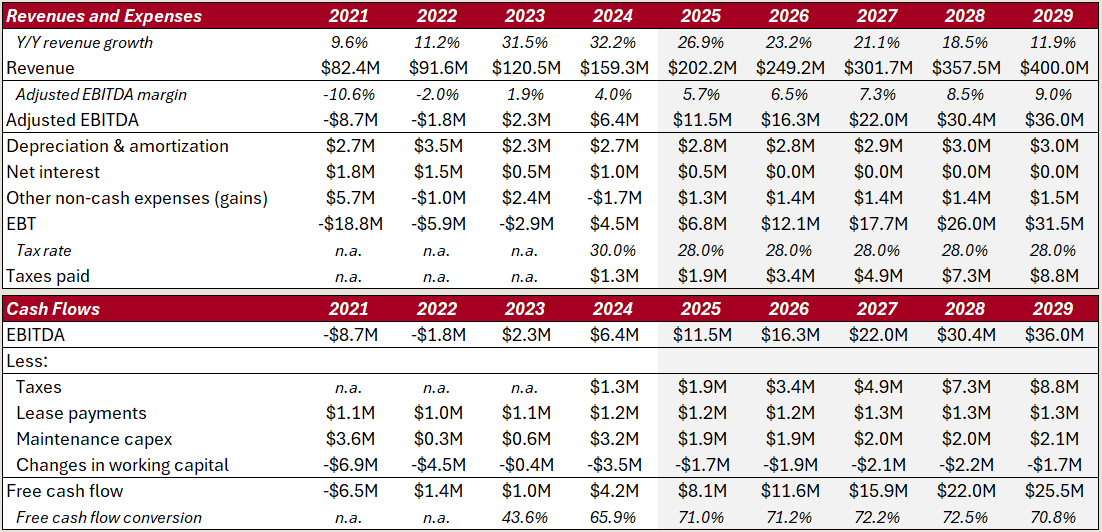

For a more comprehensive analysis of share pricing, we have built a discounted cash flows model. Figure 6 shows historical financial results alongside our estimates through to 2029. Note that the estimates shown are largely in line or above analyst’s consensus numbers, providing a somewhat bullish outlook for Kits financial prospects.

Figure 6: Financial Estimates

Source: Bloomberg, Phi Research

Revenue growth is expected to remain strong in the coming years, however at a declining rate as the costs of acquiring new customers and e-commerce penetration increases. By 2029, we anticipate that the Canadian online eyecare market will be near maturity, with a previously discussed penetration level of ~25%. At a constant market share, which we believe is a bullish scenario for Kits, this represents roughly a doubling in revenue to ~$400M per annum. With marketing spending IRR’s already likely less than 9%, increasing e-commerce penetration will only worsen this. Increasing e-commerce penetration will only decrease marketing spending IRR’s (from currently dismal levels), meaning that marketing spending as a percentage of revenue will fall over time. Subsequently, EBITDA margins may rise up to ~9% in 2029, just shy of what we see as a bullish “maturity level” for Kits (10-11%). Beyond 2029 growth is likely to slow into the single digits range and stabilize, making us confident that the use of an exit multiple is appropriate in our cash flows model below.

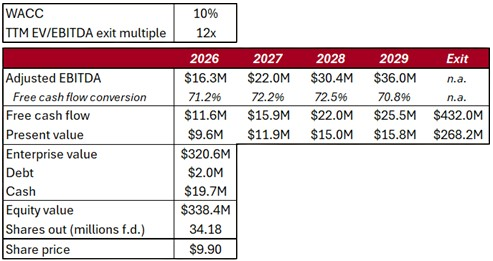

Figure 7: Discounted Cash Flows Model

Source: Phi Research

Our base case uses a 12x EV/TTM EBITDA exit multiple, indicative of a company with persistent high single digit to low double digit growth prospects and a slightly above average cost of capital. Estimating a cost of capital for Kits is tricky, as the company has only been listed for five years and has been subject to large and persistent share declines in the past. This situation yields a beta of 0.26 for the equity, a value which is undoubtedly inappropriately low. Consumer goods e-commerce names like Aritzia (TSX: ATZ, beta = 1.65) and Canada Goose (TSX: GOOS, beta=1.82) tend to exhibit betas in the range of 1.5-1.8, representing a cost of equity of approximately 11-12%. Although Kits is similar to these businesses, it is not a pure consumer cyclical; even in economic downturns consumers need contacts, and glasses spending will be more resistant to broad scale market turmoil than something like clothing due to both insurance coverage and changes in prescriptions. Pure healthcare products companies tend to exhibit betas in the range of 0.5, which would represent a cost of capital of roughly 6%. Interestingly enough, Warby Parker (Nasdaq: WRBY), Kits’ closest comp, exhibits a very high beta of 2.06 (cost of capital approaching 14%). Because of these broad ranges, we will analyze cost of capital in our sensitivity analysis in Figure 8. We believe that Kits’ represents a slightly riskier investment proposition than the market average due to the level of growth the company anticipates, small cap liquidity risks, and the consumer aspect of the business, partially offset by the stability provided by the Canadian eyecare spending cycle. As a result, we have chosen 10% as our base case cost of capital, a reasonable and somewhat bullish value.

Our discounted cash flows model yields an implied share price of $9.90 in our base case, representing a 44% discount to today’s closing price of $17.53.

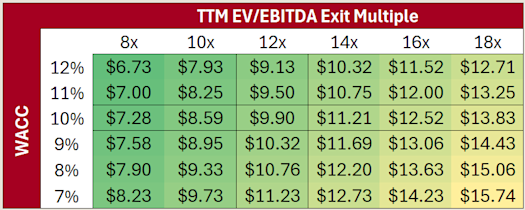

Figure 8: Sensitivity Analysis

Source: Phi Research

In our sensitivity analysis we do not find a single case in which Kits is not technically overvalued. A cost of capital of 7% is likely an unfair assessment of the risks associated with an investment in Kits, and an exit multiple of 18x is representative of some of today’s most promising long-term growth corporations, not a company in a nearly mature market with stagnating growth. We believe that our base case which yields an implied share value of $9.90 is in many ways overly optimistic and that Kits shares are significantly overvalued at current levels.

Catalysts

When making an investment in a long position with an extended time horizon, it is not extremely important to consider the short term catalysts surrounding changes in an equity’s price, as in the long term strong financial results will accrete to shareholders. When considering entering a short position, the opposite is true. Even if we can suppose that an equity is worth zero, our maximum return on such a short position is only 100%, which if spread over a long time frame has a significant opportunity cost, and funds could instead be allocated to long positions with greater returns. Because of this, we see it fit that we analyze some catalysts which will likely apply downward pressure on Kits shares in the short run.

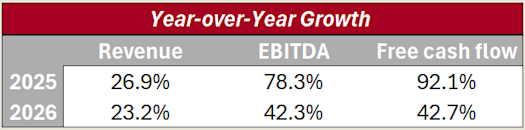

Weak Growth in 2026

As Figure 9 suggests, the rate at which Kits revenues, EBITDA, and free cash flow is anticipated to grow will be much lower in 2026 than in 2025.

Figure 9: Year-over-Year Growth Rates

Source: Bloomberg, Phi Research

Slowing growth, even if growth is still large in magnitude, is alarming to growth investors. Especially in the context of EBITDA and free cash flow, Kits has grown at very strong rates over the past two years, driving somewhat of a hype and momentum effect. A change in growth rates is a reminder to investors that a ceiling exists for the cash flow which an equity can actually generate, and forces investors to ponder the question of what should actually be priced into the equity. As we have already demonstrated, far too much future cash flow is priced into KITS at present.

Weak Q4-2025 and Q1-2026 EBITDA Estimates

Analyst’s consensus has Kits Q4-2025 EBITDA levels estimated at $2.5M as compared to actual levels of $4.9M in Q4-2024. This represents a somewhat eye-popping -49% change in EBITDA year-over-year assuming that estimates are correct. Given that analysts have lowered their estimates for Q4-2025 in recent weeks and months, we anticipate a weak quarterly EBITDA performance from Kits in Q4-2025 (reporting March 4th, 2026), regardless of if estimates are beaten. In small cap equities, year-over-year growth tends to drive share price reactions to earnings on growth stocks, not how financial performance compared to analyst estimates.

In Q1-2026, Kits is estimated by analysts to generate $3.1M in EBITDA, representing a 0% change compared to Q1-2025. Although not as poor as Q4-2025 decline rates, a 0% change in EBITDA year-over-year in a stock that trades at over 50x EV/EBITDA is sure to garner a negative response. It is also reasonably foreseeable that Q1-2026 estimates are cut in the wake of Q4-2025 results, as poor results often yield such reactions from analysts and Q1-2026 estimated EBITDA levels have been falling in recent months. The idea of estimates trends leads us nicely into our next catalyst.

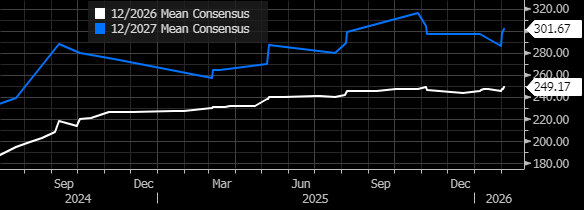

Poor Estimates Trend

Analyst’s long-term estimates are not perfect and are frequently adjusted surrounding earnings events. In recent years, Kits 2026 and 2027 revenue estimates have grown handsomely, while EBITDA estimates have remained virtually unchanged and have even sloped downwards since 2024.

Figure 10: Kits Revenue Estimates over Time

Source: Bloomberg

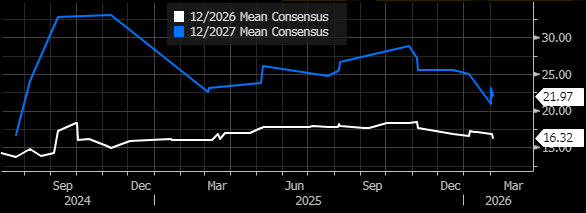

What this equates to is falling EBITDA margin estimates over time, something very alarming to investors in what is essentially a “margin expansion story”.

Figure 11: Kits EBITDA Estimates over Time

Source: Bloomberg

We do not expect EBITDA margin estimates to increase in the context of our competitive analysis on Kits, and we believe that a ceiling on revenue growth exists not far beyond 2027. At a certain point, this sentiment reaches excessively bullish investors through analysts estimates.

Lack of Margin Expansion Going Forward

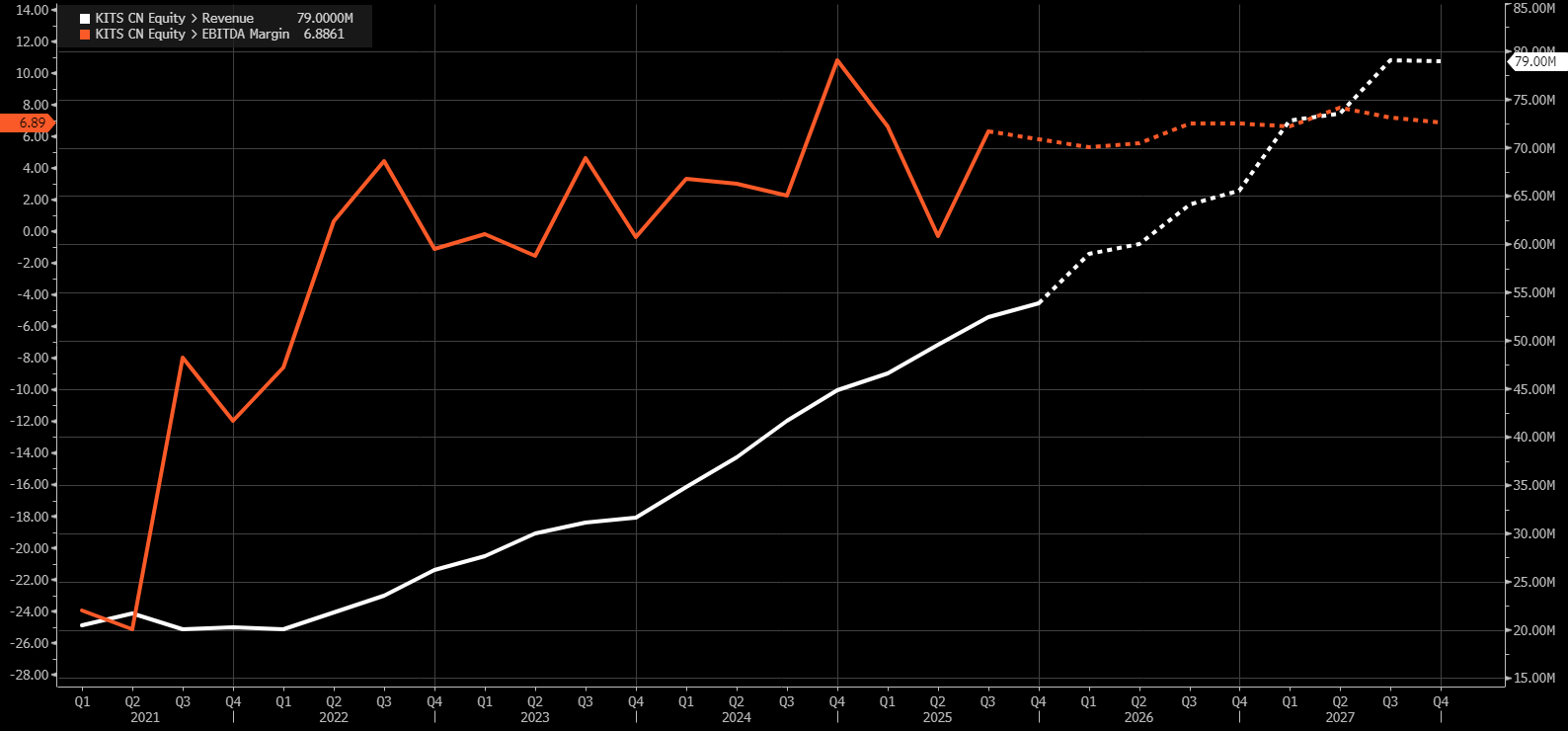

Kits is indeed a “margin expansion story”; although revenue growth is a significant driver of cash flow gains, small increases in margins can play a much more significant role in the growth of cash generation capabilities. Figure 12 shows Kits’ EBITDA margin (orange line, left axis) and revenue levels (white line, right axis) on a quarterly basis over time. The sections of solid line represent actual results, while the dotted sections are analyst’s consensus estimates.

Figure 12: Revenue and EBITDA Margin over Time

Source: Bloomberg

Analyst’s estimates do not seem to account for any significant EBITDA margin expansion in the future beyond current levels. Given this information and our well established beliefs on Kits competitive standing and business model, it may be true that Kits’ margin expansion story is essentially played out at this time. A combination of financial results and analyst revisions should solidify this fact with shareholders in the near term, and a reset of expectations for growth will have an unambiguous negative impact on Kits’ valuation.

Conclusion

Kits Eyecare Ltd. is not a worthless company, but it would appear that there is a large and growing disconnect between its investor’s expectations and reality. In general, we have written our previous reports about the positives we see in a company, but instead this report is about what we don’t see. We don’t see a competitive moat around the business, we don’t see a properly motivated or impressively qualified management team, and we don’t see the stock being worth half as much as it is in the market at present. For these reasons and given the near term catalysts we expect to apply downward pressure on shares, we believe that Kits will significantly underperform the broad market in the near term and long term. Short sell.