Westshore Terminals Investment Corporation (TSX: WTE), Riding the Incoming Tide

Published on 2025-05-31

Westshore Terminals Investment Corporation operates North America’s largest coal export terminal, located near Delta, British Columbia. The company is currently developing its facility to allow for the addition of approximately 9 million tonnes of potash exports per year (currently exporting ~26 million tonnes of coal per annum or Mtpa) in a partnership with BHP Group Ltd. We believe Westshore is a one of a kind asset and presents investors with a unique and attractively valued investment opportunity.

The Westshore business model does not involve the purchase or sale of coal or potash, the company is simply a service to North American mining companies. Raw materials are transported to the marine terminal by rail car where, upon arrival, materials are stored and loaded onto large interoceanic ships. Westshore charges mining companies a handling rate per tonne of coal loaded which generates the large majority of revenues. Figure 1 shows an overhead view of the terminal and a typical coal loading scene:

Figure 1: Terminal Overview and Loading Process

Source: Westshore Terminals

North American coal mining companies produce both thermal and metallurgical coal for export to countries worldwide. Thermal coal use cases are found in the production of heat and electricity, which, in developed nations, is slowly being phased out. Metallurgical coal is used for the production of iron and steel and currently has no viable substitutes. Roughly two-thirds of Westshore’s export volume is thermal coal, with the rest accounted for by metallurgical coal.

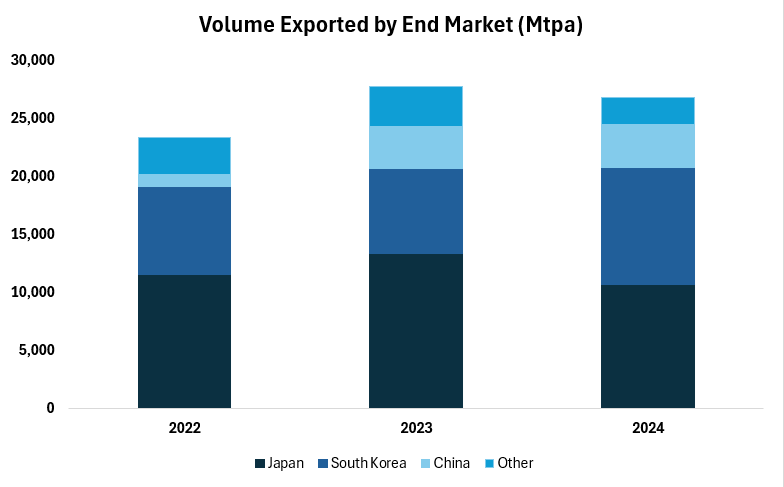

Westshore’s customers currently export to ~14 countries, with Japan, South Korea, and China demanding the highest percentage of volumes. Figure 2 shows Westshore’s export market’s respective volumes over the past three years. Countries placed within the “Other” category include India, Taiwan, Vietnam, and various European and Central & South American nations.

Figure 2: Geographic Distribution of Export Markets

Source: Company Filings, Phi Research

BHP Jansen Potash

BHP Group Ltd. is a global producer of copper, metallurgical coal, nickel, iron ore, and potash. On August 17, 2021, the company approved a $7.5M CAD investment into the first stage of its Jansen potash mine. Located in Leroy, Saskatchewan, the Jansen mine is set to have the lowest costs of production versus any comparable operation. As per BHP, population growth and increased development of crop production is poised to grow global potash demand by ~70% by 2050, an opportunity which a bundle of Saskatchewan based mining operations are taking advantage of. Saskatchewan is home to ~45% of global potash reserves, making Canada the worlds primary potash exporter.

BHP’s Jansen mine project has been divided into four separate stages, each representing 4-4.5 Mtpa in production. As previously stated, phase 1 was approved in August of 2021, with production set to begin in late 2026-early 2027 and maximum output to be reached within a three-year time frame. Phase 2 of the Jansen mine was approved in October of 2023 with associated budget of $6.4M CAD and anticipated first production in 2029. Volumes are expected to ramp up over a three-year period to full capacity of 4-4.5 Mtpa thereafter, making Jansen the largest potash mine in the world. Phases 3 and 4 remain as longer-term opportunities for capital deployment, with BHP likely not taking action within the decade. If executed upon, phases 3 and 4 would bring total Jansen mine output to 16-17 Mtpa.

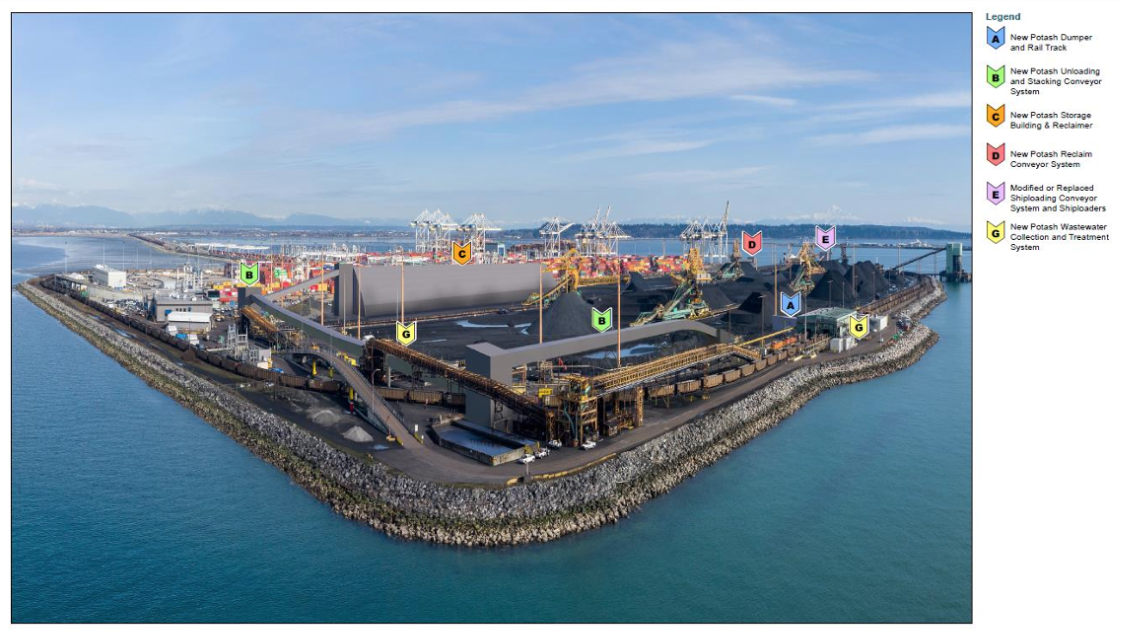

As part of the Jansen mine project, BHP has employed Westshore as its sole export terminal for associated potash. To prepare the terminal for additional export capacity of the new material, BHP agreed to invest $1B CAD in capital expenditures at the terminal. The investment goes towards a new storage building, two new conveyors, a new dumper pit and various other modifications to existing infrastructure to accommodate for small differences in potash and coal handling requirements. Figure 3 shows the modifications being made to the WTE terminal under the capital spending program:

Figure 3: Potash Expansion Project

Source: Company Presentation

The expansion is roughly 50% completed and will be on time to accept Jansen phase 1 volumes at the end of 2026. On the Westshore side, the company is required to contract all materials and associated labour to complete the construction of the above infrastructure. BHP will immediately reimburse Westshore for 95% of associated expenditures, with the remainder “held back” in receivables accounts. Upon completion of the project and commencement of export volumes flowing through, BHP will release the remaining funds to WTE. Any expenditures over the budget of $1B CAD will be at the expense of WTE alone. In contrast to Westshore’s 2007 and 2014 facility maintenance projects, the potash expansion project is expected to be over budget by 22.5%, representing a $225M growth capex contribution from WTE. Westshore largely attributes the budget overage to unexpectedly high inflation levels, which had a cumulative effect on the CPI of ~15% between the initial budget plan and today’s date. In total, $545M of the expected $1.2B of spend has been completed, with 2025 and Q1-Q3 2026 spend largely representing labour costs for completion of the project.

Phase 2 of the Jansen mine also requires additions to the Westshore facility. In comparison to phase 1 the budget is much smaller at ~$150M CAD, with funds being used to expand the storage facility built in phase 1 (object C in Figure 3). Phase 2 spending will employ an identical budgeting mechanism as phase 1, with 5% of funds being held back and released in conjunction with export volumes ramping up. Phase 2 construction will be completed by late 2029.

The agreement with BHP requires for Westshore to provide potash export services until 2051, subject to extension. BHP has provided Westshore with minimum annual export volume commitments in accordance with phase 1 mine output, with corresponding increases in minimum annual volumes as phase 2 outputs ramp up. Handling rates for potash are similar to those for coal, with the BHP agreement offering fixed handling rates which are tied to the CPI.

Competitive Landscape

For the last ten years, Westshore’s coal export volumes have been relatively unchanged with few material changes to contracts. The nature of Westshore’s business is such that a small number of customers account for almost the entirety of revenue produced. Westshore currently has agreements with 6 different customers. We believe that an analysis of the competitive landscape is one of the most important steps in assessing the security of Westshore’s contracts going forward.

The competitive landscape for dry bulk export terminals is relatively small. This is a result of a variety of factors including the requirement for large upfront investment in construction, high maintenance capital expenditures, a strict regulatory environment, and significant economies of scale in operations.

Coal Export Competitors

Westshore has two competitors for coal exports on the West Coast of North America. Both terminals are privately held and operate in British Columbia.

Trigon Pacific Terminals

Trigon Pacific Terminals is located in Prince Rupert, British Columbia, ~750km north of Vancouver. Figure 4 shows Trigon’s geographic positioning relative to Vancouver (Vancouer located at bottom of image). The terminal is situated at the pin in the image.

Figure 4: Trigon Geographic Positioning

Source: Google Maps

Trigon exports both thermal and metallurgical coal, as well as a variety of other commodities. Due to the requirement for rail transport of coal, the export terminal which is most geographically proximal to mines generally offers the lowest total costs of exporting. Consequently, Trigon largely services mines in the northern areas of Canada.

Neptune Bulk Terminals

Neptune Bulk Terminals is located ~35km north of Westshore Terminals in Northern Vancouver, British Columbia, and exports both metallurgical coal and potash. Neptune’s coal capacity is used exclusively by Elk Valley Resources (EVR), a large metallurgical coal producer located near Sparwood, British Columbia. EVR moves ~12.5 Mt through Neptune on a yearly basis. The remaining balance of metallurgical coal produced by EVR is sent to Westshore, roughly 5-7 Mtpa, representing the majority of their metallurgical coal volumes. Elk Valley Resources is owned by both Glencore and Teck Resources, with EVR holding joint ownership in Neptune Terminals with potash exporter Canpotex.

Potash Export Competitors

The majority of potash volumes produced in Saskatchewan and exported on the West Coast are marketed and delivered by Canpotex (short for Canadian Potash Exports). Canpotex is jointly owned by Mosaic and Nutrien, who cumulatively own 9 of 11 producing potash mines in Canada. Canpotex subsequently owns stakes in two export terminals on the West Coast of Canada and the United States.

Neptune Bulk Terminals

As previously stated, Neptune is jointly owned by Canpotex and Elk Valley Resources. Neptune handles the majority of Canpotex export volumes on a yearly basis, which we estimate to be ~17.5 Mtpa (assuming Neptune is running near capacity).

Portland Bulk Terminals

Portland Bulk Terminals is a wholly owned subsidiary of Canpotex located on the south shores of the Columbia River, Oregon. The Portland facility is set up for efficient handling of specialty potash products like white potash. After an expansion project in 2018, Portland Bulk Terminals now has an export capacity of roughly 7.5 Mtpa.

Analysis

The majority of Westshore’s coal volumes face contract renewals at year end 2027 and 2028. Westshore’s agreement with Elk Valley Resources, recently renewed at the end of 2024, expires in 2027. EVR only exports through one other terminal, Neptune, which it is a partial owner of. It is reasonable to assume that EVR would prioritize volumes flowing through Neptune, however, with Neptune operating at or near capacity and the requirement to share capacity with joint owner Canpotex, there is little room for increasing throughput. Additionally, given the location of Neptune in the center of Vancouver, terminal expansion would be subject to a high degree of scrutiny, and it would be unlikely that Neptune would be able to act on any new construction which influenced ocean bottom. Given the capital intensity of the industry, expansion of the Neptune terminal to replace Westshore volumes would likely be much more costly than utilizing the infrastructure which Westshore has in place. From a risk management perspective, having access to multiple terminals has significant strategic rationale to hedge against terminal outages (a somewhat regular occurrence considering the likelihood of accidents when operating large ships in tight quarters). It also seems highly unlikely that EVR cut output in the near future, as there are currently no alternatives to the metallurgical coal which it produces and demand is only set to increase. For these reasons, we see WTE’s contract with EVR as being very stable for the foreseeable future.

Westshore has a total of 5 thermal coal clients who operate across British Columbia, Alberta, and the Western United States. One such client is Navajo Transitional Energy Company (NTEC), with contracts set for expiry on December 31, 2028. NTEC produces thermal coal out of a basket of mines based in Montana, Wyoming, and Nevada. Considering the complete lack of coal export terminals on the West Coast of the United States, the only alternative for NTEC (or any thermal coal producer in the Western United States) would be Trigon Terminals in Prince Rupert, British Columbia. Considering the extensive distance which would be added to rail car travel, as Prince Rupert is almost 800km north of Vancouver, it seems highly unlikely that Trigon be able to abstract any American thermal volumes from Westshore. In general, we see Westshore’s thermal coal contracts as secure on a go forward basis.

On the potash front Westshore’s only client is BHP. Considering the investments which BHP is making in the Westshore facility (a total of $1.15B CAD confirmed for phases 1 and 2), and the guarantees set out for minimum annual throughput volumes in their agreements with WTE, it seems highly unlikely that BHP defer to a competitor. Additionally, all other potash export terminals are owned either in part or in whole by Canpotex, a company who is disincentivized to collaborate with BHP considering it is owned by their competitors. In the near term we see potash export capacity being a pinch point for the industry, with current facilities running at or near capacity and Nutrien actively seeking new terminals for additional volumes (link). Considering the forces at play, we see Westshore’s forecasted potash export volumes as very secure, with strong opportunity for future growth on the horizon.

Global Coal Demand and Local Regulatory Factors

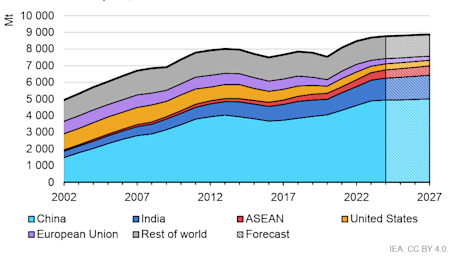

Coal is a notoriously controversial commodity due to the emissions associated with its combustion. For these reasons developed nations have made steps away from employing the use of coal for heat and power generation. As per the IEA, coal demand in developed economies has dropped by ~50% since 2007, or ~3.5% on an annualized basis. On the contrary, many developing nation’s demand for coal is growing as their requirements for power and industrial activity increases. On a global scale the IEA expects for coal demand to increase slowly up to 2027 at which point it will plateau. Figure 5 shows IEA forecasts for global coal demand through to 2027:

Figure 5: Global Coal Demand

Source: IEA

Westshore’s primary coal markets are Japan and South Korea, cumulatively representing 78% of 2024 export volumes and 99% of volumes exported to highly developed economies. Japan and South Korea accounted for 69% of metallurgical coal volumes, which we do not consider to be at risk demand, leaving Westshore ~14.7 Mtpa of at risk, first world, thermal coal demand on the table. In Japan and South Korea, the IEA has published estimates for a decrease in thermal coal demand of ~4.3% per year going forward, with a large portion of coal power being replaced by nuclear reactors. Note that the IEA has historically shown a bias towards underestimating fossil fuel demand.

Local regulatory factors could also present risks to Westshore’s business. In 2021 the Trudeau government made a statement suggesting that the end of thermal coal operations in Canada be set for 2030. There has been no further effort made by government agencies to see this through, with Westshore management confirming via communications with relevant government parties that no progress has been made towards such goals. Instead, the Canadian government has approved a number of new coal mining projects over the course of the last four years, including approval of the Grassy Mountain Coal Project in the Crowsnest Pass, Alberta, in May of this year. Overall, we could see the approval of mining projects slowing down in the years to come, but considering the extensive time frame of recently approved projects the risk of an export ban on coal is, for all practical purposes, zero.

Local regulators may also play a role in the competitive landscape surrounding Westshore. Terminal expansions are subject to a high level of scrutiny, with the primary issue being influence on estuary and seafloor habitat. Overall, we could see such scrutiny as a competitive advantage for Westshore. Local regulation has prevented the construction of any coal export infrastructure on the West Coast of the United States in the past, and all signals point towards this remaining unchanged going forward. On the potash front, Westshore is much more secluded in comparison to Neptune Terminals and Portland Terminals. Additionally, Westshore is an offshore terminal and is not located on land or in close proximity to urban areas. This means construction associated with expansions will yield much less noise and disturbance for urban residents which increases the probability of project approvals. Additionally, Westshore’s geographic positioning leaves a much larger area for expansion in comparison to Neptune and Portland Terminals.

Valuation

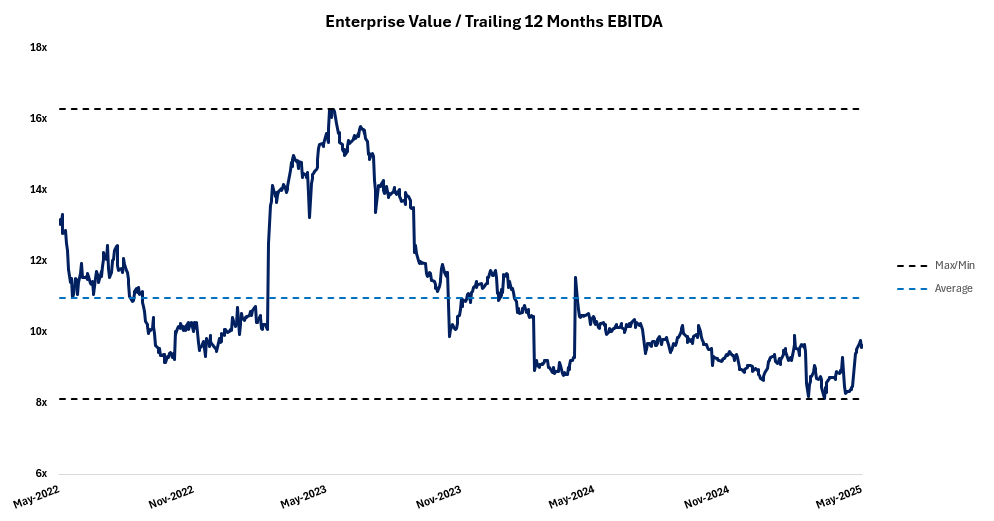

With the knowledge we have accrued we can now make a critical assessment of share value. On an enterprise value to trailing 12 months EBITDA basis, shares are trading at ~9.6x, below the three-year average of 11.0x and above the three-year low of 8.1x. Figure 6 shows WTE’s relative valuation over the past three years:

Figure 6: Enterprise Value / Trailing 12 Months EBITDA

Source: Capital IQ

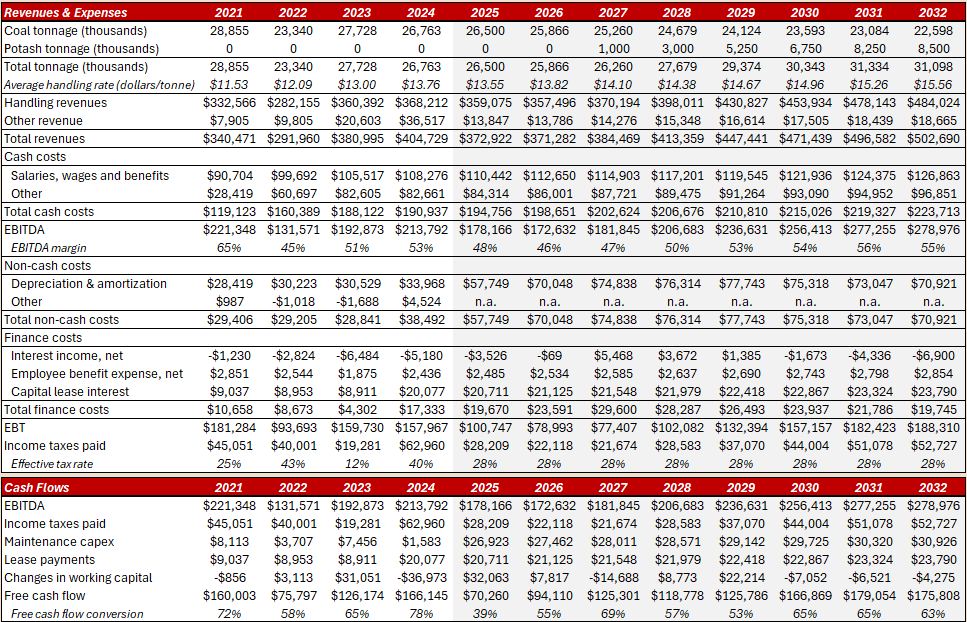

On a multiples basis shares appear to be attractively valued. For a comprehensive analysis we will build a full cash flow model. Figure 7 shows historical results along with our estimates through to 2032. Note that values are in thousands of Canadian dollars unless specified otherwise.

Figure 7: Financial Forecasts

Source: Company Filings, Phi Research

Due to the nature of their business, Westshore has a strong line of sight into current year coal volumes and handling rates which they estimate at 26.5 Mtpa and $13.55 for the year respectively. Going forward we have forecast for coal volumes which we designated as “at risk” to decline by ~4.3%, in line with the IEA’s estimates, with exports of metallurgical coal and those to undeveloped economies remaining flat. Note that an annual 4.3% decrease in coal demand would represent a nearly 25% decrease in demand from 2025-2032. Potash volumes from phase 1 of the Jansen project will begin flowing in 2027 at 1 Mtpa and will ramp up to 4.25 Mtpa by 2029. Phase 2 volumes will begin flowing in 2029 and will ramp up to 4.25 Mtpa in 2032, all in line with BHP and Westshore expectations. Handling rates are tied to inflation and are approximately the same for coal and potash.

Westshore’s cost structure consists almost entirely of fixed costs, granting the company significant operating leverage as total export volumes grow. Most employees are members of labour unions, for which salaries are tied to the CPI. In alignment with the ramp up of Jansen potash volumes WTE EBITDA margins should expand significantly.

Westshore currently has ~$136M in cash for which it earns interest. We have estimated interest income and expense based upon Westshore’s requirement for debt financing in 2027 to complete Jansen phase 1 expansions. Upon prioritizing debt repayment as a use of free cash flow (apart from dividend payments) Westshore will be able to fully deleverage by 2030.

Westshore has spent very little on maintenance capex in the last four years as a result of emphasis being placed on the potash expansion project. To estimate maintenance capex on a go forward basis we have analyzed Westshore’s capital expenditures from 2007-2019, during which time two equipment maintenance projects were undertaken. Westshore deployed $110M on maintenance activities from 2007-2012 and $240M in their 2014-2019 program. Distributed evenly across the 13-year period this is roughly $26M per year. We have utilized this value with adjustments for inflation going forward. Although equipment maintenance expenditures will likely be somewhat lumpy and project based, as they were in the 2007 and 2014 maintenance projects, we believe our estimates accurately reflect the requirement for capital expenditures in aggregate and if anything offer a conservative view of future free cash flows.

Historically Westshore’s lease payments have been tied to total export volumes, however the company has revised its lease agreement as of late to be fixed and to grow roughly in line with inflation. Non-cash working capital accounts have historically held a negative balance, floating in between -10% and -15% of annual revenue. 2023 and 2024 have seen a deviation from this trend as a result of the Jansen potash expansion which has driven up accounts payable. WTE is scheduled to make the majority of payments to suppliers as export volumes begin flowing and we estimate that working capital accounts will return to ~-12% of annual revenue by 2029 without accounting for holdback payments received from BHP. Holdbacks on expansion expenditures currently sit in long term receivable accounts and will be released in conjunction with the ramp up of potash export volumes.

The result of our analysis is a steadily growing free cash flow base from 2025 onwards. Figure 8 shows our discounted cash flow model expressed in millions of Canadian dollars:

Figure 8: Discounted Cash Flow Model

Source: Company Filings, Phi Research

We have utilized an enterprise value to trailing 12 months EBITDA exit multiple of 11x for our terminal value and calculated WACC of 7.95% using the Capital Asset Pricing Model and a beta of 0.99. Our exit multiple is roughly reflective of the previous three-year period average. WTE currently has $136M in cash and zero debt, however we have not used these values in converting current enterprise value to market cap. Recall that phase 1 of the BHP potash expansion is estimated to be over budget by $225M for which Westshore is solely responsible. We have not included this spending in our maintenance capex forecast as the purpose of the expenditures is a scope expansion project. To account for such expenditures in our valuation we have estimated Westshore’s requirement for debt and the use of current cash to fund the potash expansion. After expenditures have been made, we forecast a cash balance of zero and a debt balance of $78M. Westshore currently has zero debt and no estimates for a cost of debt, meaning we do not have any basis to include their cost of debt in our WACC calculation. Ultimately inclusion of this in our valuation process would have limited impact on share price based on the small weighting of debt in total capital structure. Cost of debt financing will also be lower than cost of equity meaning that our approach will provide a slightly more conservative estimate of intrinsic value than one where we alter our WACC.

Under our set of assumptions we estimate that shares should be worth $35.24, 32% higher than Friday’s close of $26.65. Including a $1.50 yearly dividend (~5.6% yield on Friday’s close), this implies an attractive opportunity for returns.

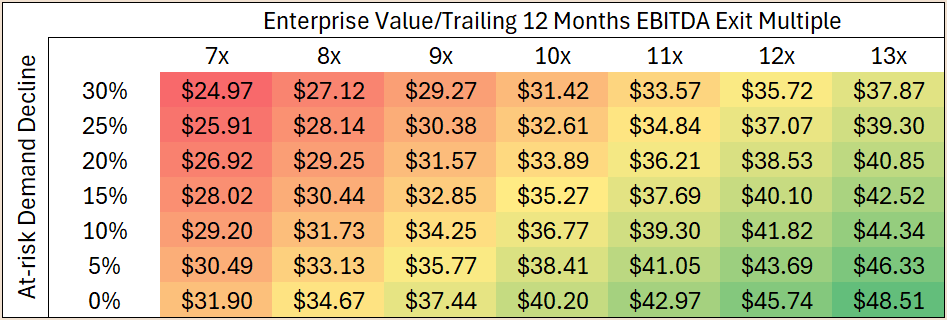

Our valuation, on a relative basis, is not sensitive to changes in inputs. The two most important assumptions made, and least rigorously justified, are the exit multiple used and the decline rate for at-risk coal demand over the next seven years. For the sake of sensitivity analysis we have prepared a table showing the intrinsic value of shares under a variety of assumption sets, shown in Figure 9.

Figure 9: Sensitivity Analysis

Source: Phi Research

For exit multiples we have included values ranging from 7-12x enterprise value to trailing 12 months EBITDA. Note that the three-year low for such values is 8.1x and, and the three-year average is 11.0x (see Figure 6). Excluding pandemic lows, Westshore has only traded below 7x for ~8 months in the last ten years, averaging a multiple of ~9x in the same period.

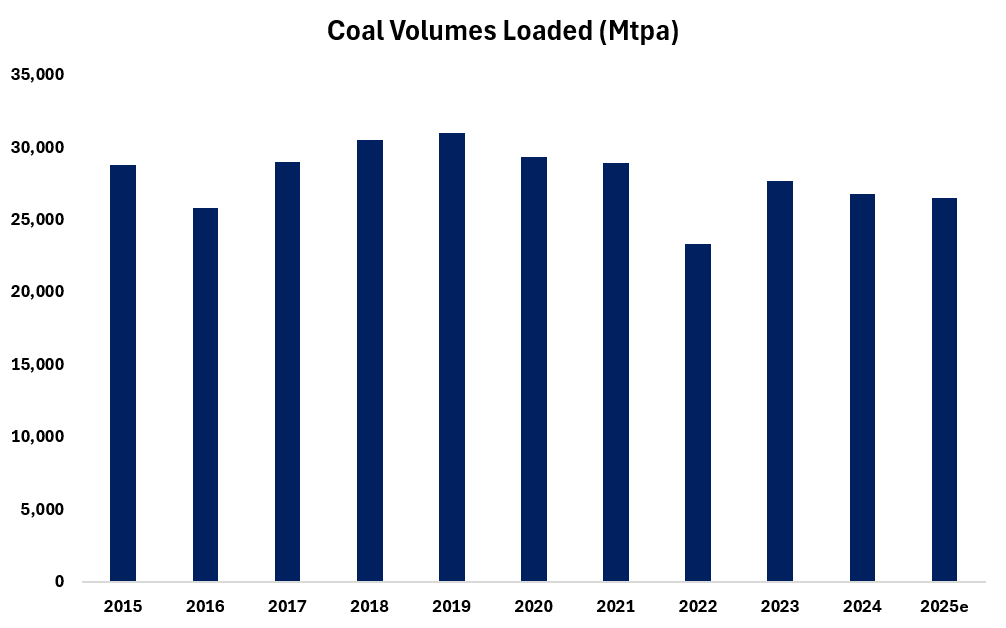

For at-risk demand decline our base case was roughly 25%, representative of the IEA forecast of a 4.3% decline in demand on an annual basis from 2025-2032. The IEA frequently underestimates demand for fossil fuel consumption and is a notoriously biased agency, meaning we see most reasonably foreseeable scenarios showing less coal demand decline than anticipated. Increasing electrical output is a key challenge facing the world and the majority of emerging technologies like artificial intelligence and electric vehicles. It is difficult to picture first world nations cutting electricity production with coal by a large margin when demand for electricity is a pinch point in the development of their economies and their socioeconomic standing. Figure 10 shows Westshore’s total coal export volumes from 2015-2025, which have decreased at an annualized rate of less than 1% in the period.

Figure 10: Westshore Coal Exports Over Time

Source: Company Filings, Phi Research

Overall we see significant upside in shares in almost every reasonably foreseeable scenario. Even in our most pessimistic analysis, dividends received for the year would accommodate for any losses in share value.

Summary and Investment Decision

Westshore Terminals is truly a one of a kind asset. When considering the forces at play on both a macro and micro level we are more than comfortable with our financial analysis and think shares in WTE are a worthwhile investment. Westshore may not be a get-rich-quick scheme, but it is far from a sleepy dividend investment. We do not see the production and export of coal in Canada lasting forever, but it will take time for demand to subside on a global scale. BHP Jansen phases 3 and 4, the speed and timeline of growth in Canadian potash exports over the next 40 years, and the current lack of infrastructure which is available to meet these exports all create a significant backstop against any declines in coal demand and could feasibly create opportunities for expansion within a short time frame. We like the stability of the asset, we like the valuation, and we like the outlook in the five, ten, twenty, and even fifty-year time frames. Strong Buy.