Exiting Position – Superior Plus Corp. (TSX: SPB)

Published on 2026-04-23

Today, shortly before market close, we exited our position in Superior Plus Corp. (TSX: SPB) at a realized price of $7.47. Our decision is a function of weak results from the Superior Delivers cost savings framework thus far and uncertainty surrounding the validity of the initiative going forward.

We initially published our thesis on Superior Plus Corp. in late May of 2025 (link), marking the first report to be put out on PhiResearch.ca. Our thesis at the time was relatively straightforward: SPB had established what appeared to be a credible and achievable set of cost savings initiatives; including data driven route optimization and use of midstream infrastructure, rerouting of yearly deliveries away from peak seasons, and the employment of churn prediction tools, none of the upside from which was reflected in share prices. Nearly a year later, results of these initiatives have been somewhat underwhelming with little explanation surrounding why. Ultimately, backward looking performance is not indicative of the future of the Superior Delivers framework, but the lack of execution thus far, the pushing back of timelines associated with financial goals, and the lack of clarity surrounding the future of the program makes it difficult for us to estimate the future of SPB’s financials and subsequent share returns. Although shares are priced somewhat attractively in the case that the program is successful, we do not believe our insights into the success of the program is sufficient for SPB to be an investable thesis at this time. In the event that investors receive clarity on the situation, we would consider a position in SPB once again.

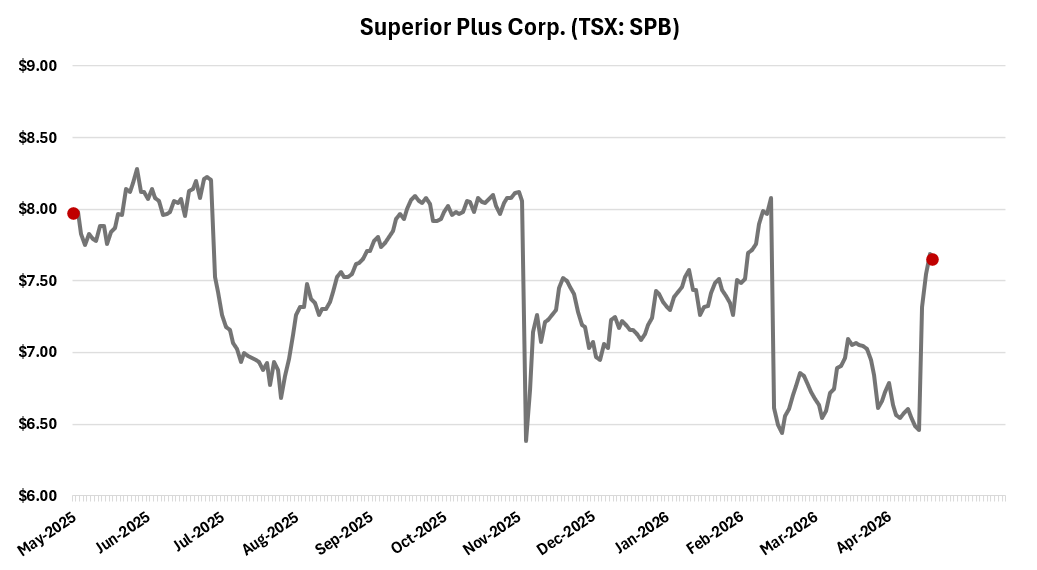

In the past 11 months, what has played out for Superior Plus has been somewhat of a worst case scenario: propane volumes were weaker than expected, CNG volumes were down in response to weak Permian drilling activity, and the Superior Delivers program disappointed both from a 2025 results perspective and in relation to changes in future expectations. At the time that we published, we believed that SPB shares presented very little downside in the event of poor execution. Luckily this expectation was correct, with our realized return coming to -4.0%, or -4.4% on an annualized basis when accounting for the reinvestment of dividends. The below chart shows the performance of SPB shares over our position’s duration including the receipt of dividends, with red markers indicating our position entrance and exit points.